In crypto markets, trades are executed under different liquidity models. One of those models is known as last look execution.

Last look affects how and when a quoted price becomes final. While the mechanism operates within milliseconds, it influences rejection rates, slippage patterns, and execution predictability, particularly in volatile conditions.

Understanding how last look works is important for brokers, funds, payment providers, and other institutional participants evaluating liquidity sources. The presence or absence of last look changes how risk is distributed between liquidity providers and trading counterparties.

This article explains what last look execution means in crypto markets, why it exists, and how it compares to no-last-look models.

What Is Last Look Execution?

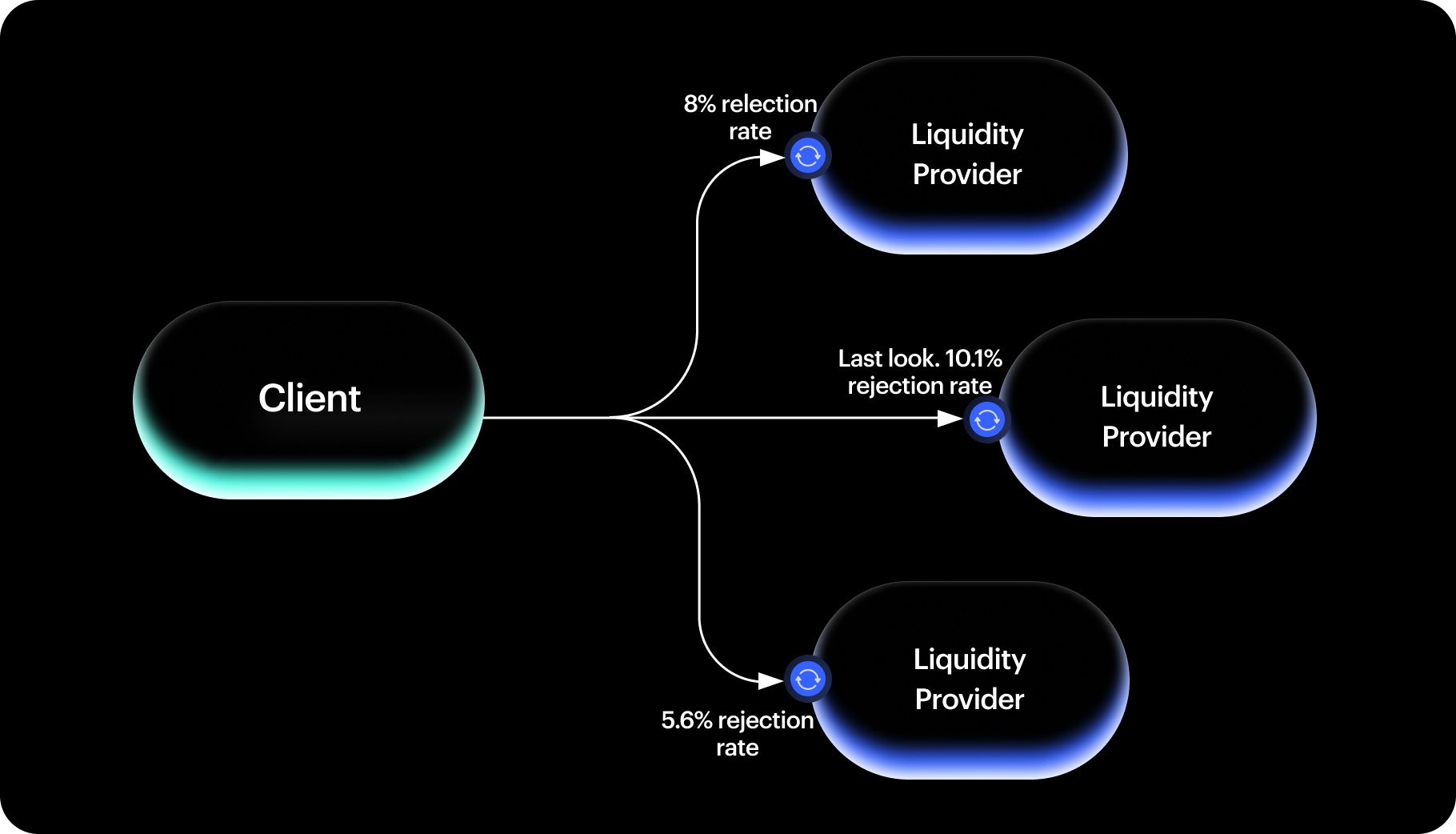

Last look execution is a trading model in which a liquidity provider retains a short validation window after receiving an order.

When a liquidity provider streams a quote and a client submits an order against that price, the order is not immediately final. Instead, it enters a brief review period, typically measured in milliseconds. During this time, the liquidity provider verifies whether the quoted price remains executable.

Liquidity providers use this window to verify their own credit limits, counterparty exposure, and internal inventory before final confirmation. If all conditions are met, the trade is confirmed at the original price. However, if any parameters exceed predefined limits or internal risk checks are triggered, the order may be rejected.

In practical terms, the process follows this sequence:

-

A liquidity provider streams a price.

-

A client submits an order.

-

The order enters a validation window.

-

The liquidity provider either confirms or rejects execution.

From the client’s perspective, the process appears almost instantaneous. However, the impact becomes visible in metrics such as rejection rates and fill consistency, especially during periods of heightened volatility.

A well-known issue in the FX market (which is highly relevant to the crypto market) addressed by the FX Global Code is the definition of ethical boundaries for the use of 'last look.' The Code categorizes any practice that prioritizes a liquidity provider's profit over client fairness as a violation of good faith. A primary concern is pre-hedging, where a provider uses information from a pending trade request to enter the market for their own account before confirming the client’s order. Additionally, the Code discourages asymmetric price checking—where trades are only rejected if the market moves against the provider—and warns against excessive latency, involving the intentional delay of the 'holding period' to observe further market fluctuations.

Last look is most commonly used in OTC and RFQ-based environments. It is less common in firm-liquidity ECN models where prices are fully committed at the time they are shown.

Execution Flow: Where Does Last Look Enter into Play?

To understand the impact of last look, it helps to place it within the broader execution process.

In institutional crypto trading, execution typically involves multiple components: liquidity providers streaming prices, aggregation systems consolidating quotes, order routing logic, and settlement infrastructure. Depending on the venue or model, orders may be matched internally, routed externally, or negotiated bilaterally.

In a last look model, the validation window appears after the order is submitted but before the trade becomes final.

A simplified flow looks like this:

-

A liquidity provider streams a bid and ask.

-

A client hits or lifts the quote.

-

The order is received by the liquidity provider.

-

The order enters a short validation window.

-

The trade is either confirmed or rejected.

The key point is that the quoted price is not fully committed at the moment it is displayed. Commitment occurs only after the validation step.

This differs from firm-liquidity environments, where executable prices are binding the moment they are matched according to price-time priority rules. In those systems, there is no discretionary review after order arrival.

In crypto markets, where liquidity is often aggregated from multiple exchanges and venues, small time differences between quote generation and order arrival can create exposure to stale pricing. Last look is inserted at this point in the workflow to manage that exposure.

While the validation window is short, its presence changes the execution profile of a venue. The effect may be minimal in stable markets but becomes more visible during sharp price moves, thin liquidity, or large order sizes.

Understanding where last look sits in the execution chain helps clarify what it does and what it does not do. It does not determine spreads or depth directly. Instead, it determines when a quote becomes a firm obligation.

Why Liquidity Providers Use Last Look in Crypto

Last look is primarily a risk management mechanism. It was introduced as electronic trading accelerated and execution speeds increased across venues.

In the crypto space, price formation happens across multiple exchanges, OTC desks, and liquidity pools. Quotes are often aggregated from several sources and distributed to counterparties through APIs and routing systems. Even in low-latency environments, small timing differences can occur between the moment a quote is generated and the moment an order arrives.

During that interval, market conditions may change.

Liquidity providers face exposure to:

-

Rapid price movements

-

Cross-venue discrepancies

-

Thin order books during off-peak hours

-

Information asymmetry between participants

Without a validation step, providers may repeatedly execute trades at prices that no longer reflect current market conditions. Over time, this can lead to systematic losses, particularly in volatile environments.

Last look allows the liquidity provider to confirm that the quoted price remains valid before committing capital. The validation thresholds are typically predefined and may incorporate price movement tolerances, order size limits, and latency parameters.

Volatility amplifies this need. Crypto markets operate continuously and are sensitive to macro news, exchange incidents, liquidations, and shifts in derivatives positioning. During these periods, prices can move sharply within milliseconds. A validation window gives liquidity providers a mechanism to manage this exposure.

It is important to note that last look does not eliminate risk. It redistributes it. The liquidity provider retains a degree of control over execution commitment, while the counterparty accepts a higher probability of rejection in exchange for tighter quoted pricing.

Whether this trade-off is appropriate depends on the use case, trading strategy, and tolerance for execution uncertainty.

How Last Look Works (and Doesn’t) in Practice

Last look is often described as a validation window, but its practical impact becomes visible only when orders interact with live market conditions.

There are three possible outcomes during this window:

-

Acceptance occurs when the market has not moved beyond predefined tolerance thresholds. The trade is confirmed at the originally quoted price, and execution proceeds.

-

Rejection occurs when the price has moved materially or when the order breaches internal risk limits, such as size constraints or latency thresholds. In this case, the trade does not execute.

-

In certain OTC or RFQ environments, a third outcome is possible: requote. Instead of rejecting the order outright, the liquidity provider may return an updated price that reflects current market conditions. The counterparty can then choose whether to proceed at the revised level.

A simplified example illustrates the mechanics.

Assume a client submits an order to buy BTC at 60,000. At the time the quote was streamed, this price reflected available liquidity. Within milliseconds, underlying exchange prices move to 60,040. During the validation window, the liquidity provider detects that the original quote no longer reflects executable conditions. The order is either rejected or requoted at the updated level. Without this validation step, the provider would be required to fill the trade at 60,000 despite the market shift, absorbing the difference.

The duration of the validation window plays a central role in how last look behaves.

These windows are extremely short, but even small differences can materially affect execution outcomes. The length of the window directly influences how risk is distributed between liquidity providers and counterparties.

A shorter window leaves less time for the market to move, increasing the likelihood that trades are accepted. However, it exposes the liquidity provider to a greater probability of executing against prices that have already shifted.

A longer window gives the provider more time to validate conditions against updated market data. This reduces their exposure to adverse price movement but increases the chance that orders will be rejected or requoted during volatile periods.

Because these thresholds are defined by each liquidity provider’s risk model, last look behavior is not uniform across venues. Differences in window duration, tolerance bands, and validation logic can lead to materially different execution statistics — even when quoted spreads appear similar.

It is also important to clarify what last look does not do.

It does not inherently widen spreads. It does not automatically create slippage. And it is not, by definition, unfair. What it introduces is conditional commitment: a displayed quote becomes binding only after passing validation.

In ECN environments, which support firm-liquidity, such as FM Marketplace, this conditional step does not exist. Prices streamed into the order book are firm and executable according to price-time priority. If a participant interacts with a displayed quote and matches within the engine’s rules, the trade is binding.

Last Look vs No Last Look: Structural Differences

The difference between last look and no-last-look models is not philosophical. It is architectural.

In a last look environment, the liquidity provider retains a post-arrival validation step before confirming execution. A quote may appear tradable, but it becomes final only after passing predefined tolerance checks. Risk is managed at the moment of trade confirmation.

In a no-last-look model, commitment occurs at the point of matching. Once a price is displayed and interacted with according to the venue’s rules, execution is binding. There is no discretionary validation window after the order arrives. Risk is managed before the quote is shown, not after the order is received.

-2.png)

This structural distinction affects several execution characteristics.

In last look environments:

-

Rejection rates may increase during volatility.

-

Quoted spreads may appear tighter.

-

Execution outcomes depend on tolerance thresholds and validation logic.

In no-last-look environments:

-

Fill certainty is higher.

-

Execution is deterministic once matched.

-

Liquidity providers must price risk proactively rather than reactively.

Neither model is universally superior. Each allocates risk differently between counterparties.

A trading desk prioritizing minimal spread in calm conditions may accept occasional rejections under stress. A market participant executing time-sensitive hedges may prioritize certainty of fill over marginal spread improvements. A payment corridor operator may require predictable execution regardless of short-term price movement.

For institutional participants, the key consideration is alignment. Execution models should reflect strategy design, flow characteristics, and risk tolerance. Evaluating rejection statistics, slippage symmetry, and fill consistency across market regimes provides a more accurate picture than simply asking whether last look is present.

The distinction ultimately comes down to one question: when does a quoted price become a firm obligation?

What Is No Last Look Execution?

No last look execution is a trading model in which quotes are firm at the moment they are shown. Once a price is streamed and matched according to the venue’s rules, the trade is binding. There is no discretionary validation step after the order arrives.

Under this structure, execution either occurs immediately or not at all. If an order interacts with a quote while it is still active and within predefined parameters, the trade is confirmed without further review. If the quote has already been updated, withdrawn, or exceeded size limits before the order arrives, the trade does not execute.

The key distinction is timing. In no-last-look environments, risk checks and exposure controls are applied before prices are made available to counterparties. Credit limits, counterparty permissions, and liquidity commitments are defined in advance. Once those conditions are met and the quote is visible, it represents a firm obligation.

This approach produces deterministic execution behavior. Market participants know that if they match against a displayed price within the system’s matching logic, the trade will settle. There are no post-arrival accept, reject, or requote decisions.

For institutions evaluating execution infrastructure, this predictability can simplify transaction cost analysis, hedging models, and performance measurement. The certainty of fill becomes a measurable property of the system rather than a variable influenced by validation thresholds.

Why Some Markets Prefer No Last Look

Certain trading environments prioritize execution certainty over conditional validation. In these contexts, deterministic behavior can be more important than marginal spread differences.

Algorithmic trading strategies, cross-venue market makers, and liquidity-sensitive hedging desks often depend on precise timing. Even small increases in rejection frequency can disrupt inventory management or offsetting trades. For these participants, the ability to rely on firm quotes reduces operational friction.

Execution transparency is another factor. In no-last-look environments, the logic is binary: either a price is tradable under defined rules, or it is not. There is no discretionary layer that introduces uncertainty after order submission. This makes it easier to analyze fill ratios and isolate performance drivers.

At the same time, removing post-arrival validation shifts responsibility to liquidity providers. Without a validation window, providers assume greater exposure to rapid price movement.

To manage this risk, they may adjust spreads, size limits, or inventory models. In other words:

No last look → higher execution certainty → greater pre-trade risk for liquidity providers

As a result, pricing structures may differ from those observed in validation-based environments. The trade-off is structural, not ideological.

Markets that prioritize predictable settlement, algorithmic precision, or cross-venue coordination often favor firm-liquidity models. Markets that prioritize conditional price accuracy during rapid volatility may accept validation windows.

Understanding these preferences requires evaluating strategy design, flow characteristics, and tolerance for execution variability. The choice between last look and no last look is ultimately a decision about when commitment becomes final, at the moment of display, or after validation.

Last Look vs No Last Look Execution In Crypto

The distinction between last look and no-last-look execution affects how risk is allocated, how prices are committed, and how predictable execution outcomes are under different market conditions.

Risk Distribution

Last Look: The liquidity provider retains partial control after an order arrives. During the validation window, the provider can confirm whether the price remains executable. Execution risk is therefore shared, as the counterparty may face rejection after interacting with a displayed quote.

No Last Look: The liquidity provider assumes full execution commitment once a quote is matched. Risk is managed before prices are shown, through inventory management, pricing logic, and credit controls, rather than after order arrival.

At its core, the difference between the two models is about when risk becomes final.

Order Acceptance and Timing

Last Look: After an order arrives, it enters a brief validation window, typically measured in milliseconds. Execution becomes binding only after the provider confirms that pricing remains within predefined tolerance levels.

No Last Look: Execution occurs immediately upon matching an active quote. If the price is visible and the order meets system parameters, the trade is final. There is no intermediary review step.

The timing of commitment, post-validation versus immediate matching, defines the execution model.

Pricing and Spread Structure

Last Look: Because liquidity providers retain a validation mechanism, they may stream tighter headline spreads. The ability to reject trades during volatility acts as a risk control layer.

No Last Look: Liquidity providers commit fully to displayed prices. Without a validation window, exposure must be managed proactively. This may result in more defensive spreads, particularly in fast-moving markets.

The trade-off is structural: conditional validation versus firm commitment.

Rejection Behavior

Last Look: Orders may be rejected during the validation window if market conditions move beyond tolerance thresholds or internal risk criteria are triggered. A tradable price at submission does not guarantee execution.

No Last Look: Rejections occur only if the price is no longer available when the order arrives or if the order exceeds predefined limits such as size or credit constraints. There is no discretionary rejection after submission.

Last look introduces conditional execution. No last look creates deterministic execution.

Transparency and Execution Clarity

Last Look: Execution outcomes depend on predefined validation logic. While structured, the presence of a review window can introduce variability during volatile conditions.

No Last Look: Execution rules are binary. If a quote is available and matched within system parameters, the trade executes. This makes fill behavior easier to monitor and audit.

Neither model is universally superior. Each distributes timing and pricing risk differently. The appropriate structure depends on strategy design, volatility tolerance, and the importance of execution certainty within the broader trading framework.

Frequent Questions about Last Look Execution in Crypto

Is last look allowed in crypto trading?

Yes, last look is widely used in OTC and RFQ-based crypto trading environments. There is no prohibition against the mechanism itself, provided it is clearly disclosed and applied consistently. The central issue is transparency. Market participants should understand whether a validation window exists, how it operates, and under what conditions orders may be rejected. Concerns typically arise only when validation logic is opaque or applied asymmetrically.

Does last look cause slippage?

Last look does not directly cause slippage. Slippage occurs when market prices move between order submission and execution. In a last look environment, significant price movement may lead to rejection or requote rather than execution at an unfavorable price. In a no-last-look environment, liquidity providers commit to the displayed price once matched, which may influence how spreads are structured. Execution outcomes depend on latency, liquidity depth, volatility, and infrastructure design, not solely on the presence of a validation window.

Does no last look guarantee better execution?

No-last-look execution guarantees deterministic fill logic, but it does not automatically result in tighter spreads or lower trading costs. By removing post-arrival validation, liquidity providers assume greater exposure to rapid price movement. To manage this risk, they may adjust spreads or size limits accordingly. Evaluating execution quality therefore requires looking beyond the validation model and considering pricing behavior, fill consistency, and performance across different market conditions.

Why do some venues offer no last look?

Venues that prioritize execution certainty often operate without last look because it provides predictable commitment once a price is matched. Deterministic execution can simplify transaction cost analysis, hedging models, and performance measurement. This structure is particularly relevant for strategies that depend on reliable fills and precise timing. The absence of post-arrival validation reduces uncertainty around whether a visible price will execute.

How can institutions assess the impact of last look?

Institutions typically evaluate execution performance by analyzing rejection rates, fill ratios, slippage distribution, and execution consistency during both stable and volatile periods. Reviewing these metrics across market regimes provides a clearer understanding of how a validation window affects outcomes. Rather than focusing on whether last look is present, institutional desks assess whether execution behavior is symmetric, predictable, and aligned with their trading objectives.

When might a trading desk prefer no last look?

A no-last-look model may be preferable when execution predictability is critical to strategy performance. This is often the case for algorithmic trading desks, cross-venue market makers, or payment flows that require deterministic settlement. In such scenarios, the certainty that a matched quote will execute can outweigh potential pricing differences. The decision ultimately depends on how a desk balances execution certainty, spread sensitivity, and volatility exposure.

(1).png)