Launching a crypto OTC desk in 2026 is no longer just a question of connecting to a liquidity provider and offering clients a quote. The market has changed. B2B clients now expect tighter spreads, reliable execution, broader asset coverage, transparent settlement workflows, and the ability to trade digital assets without taking unnecessary operational risk.

Demand for OTC execution is expanding beyond traditional crypto-native trading firms. Brokers, payment providers, fintech companies, banks, stablecoin businesses, family offices, and institutional desks are all looking for ways to serve clients who need efficient access to crypto liquidity. For many of them, the opportunity is clear: launching an OTC desk can open a new revenue line, strengthen client relationships, and support growing demand for fiat-crypto and stablecoin transactions.

But building an OTC desk is not the same as launching a simple trading interface. A competitive desk needs liquidity access, pricing logic, execution technology, compliance processes, custody and settlement workflows, reporting, risk controls, and client onboarding. Each of these elements affects the quality of service clients receive — and, ultimately, whether the desk can scale.

This guide explains how to launch an OTC desk, what infrastructure is required, and how businesses can choose between building the stack internally or using white-label OTC desk infrastructure. It also covers the main operational decisions, common mistakes, and the role of institutional technology providers such as Finery Markets in helping companies bring OTC trading services to market faster.

What is a crypto OTC desk?

A crypto OTC desk is a trading service that enables clients to buy and sell digital assets directly with a counterparty, instead of placing orders on a public exchange order book. OTC stands for ‘over-the-counter,’ meaning trades are arranged bilaterally or by sourcing liquidity from various trading venues, often with pricing provided by liquidity providers, market makers, or internal trading teams. Unlike public exchange trading, crypto OTC trading is built around private price discovery, negotiated execution, and post-trade coordination.

In crypto markets, OTC desks are commonly used for larger or more complex transactions where execution quality matters. A client may want to trade Bitcoin, Ethereum, stablecoins, or fiat-linked pairs without moving the market, exposing the full order size to an exchange, or managing execution across multiple venues themselves. The OTC desk acts as the access point: it provides prices, executes the trade, and coordinates the post-trade process.

OTC desks are used by a wide range of institutional and professional clients, including brokers, payment providers, hedge funds, family offices, crypto companies, fintechs, banks, and businesses that need to convert between fiat currencies, stablecoins, and digital assets. For these clients, OTC trading is not only about size. It is also about certainty, relationship-based execution, and operational simplicity.

Crypto OTC desk vs exchange execution

The main difference between an OTC desk and an exchange is how the trade is executed. On a centralized exchange, a client usually interacts with an open order book where prices and available liquidity are visible to the market. The final execution price depends on the order size, market depth, and available liquidity at the time of execution.

With an OTC desk, the client typically requests a quote for a specific asset, size, and trading pair, or views a stream of quotes from liquidity providers tailored to their specific needs. The desk then provides a price based on its liquidity access, internal risk model, and market conditions. Once the quote is accepted, the trade is executed according to the agreed terms.

This model is especially relevant for institutional and corporate clients because it can reduce market impact, simplify execution, and provide a clearer trading workflow. Instead of splitting orders across exchanges or managing multiple accounts, clients can rely on a single OTC desk to source liquidity, provide pricing, and support settlement.

Why launch an OTC desk in 2026?

OTC execution is becoming a more central part of institutional crypto market structure. According to Finery Markets' 2026 institutional OTC trading outlook, institutional spot OTC volumes expanded by 109% year over year, compared with just 9% YoY growth across the top 20 centralized exchanges by the end of 2025. The same report found that 40% of surveyed institutions now name OTC as their first-choice execution venue, routing more than half of their trades off-screen.

This shift reflects a broader change in how professional clients access digital asset liquidity. In earlier crypto market cycles, OTC desks were mostly associated with large Bitcoin trades, hedge funds, miners, and crypto-native institutions. In 2026, the use case is broader. OTC infrastructure is now relevant for brokers adding digital assets to their product offering, payment providers handling fiat-stablecoin flows, fintechs serving cross-border clients, and banks or EMIs exploring regulated access to crypto liquidity.

Stablecoins are also changing the role of OTC desks. Their share of institutional OTC transaction volume rose from 23% in 2023 to 78% in 2025, turning them from a bridge asset into one of the dominant settlement instruments in institutional crypto markets. For businesses serving payment, treasury, brokerage, or cross-border transaction flows, this creates demand not only for crypto-to-crypto execution, but also for reliable conversion between fiat currencies, stablecoins, and major digital assets.

For many firms, the opportunity is not simply to “offer crypto trading.” It is to become the execution layer their clients already need. A well-structured OTC desk can help companies expand wallet share, increase transaction revenue, improve retention, and support more complex institutional workflows without sending clients to third-party exchanges.

What do you need to launch an OTC desk?

To operate competitively, a desk needs a full execution workflow: liquidity access, price discovery, trading technology, settlement processes, compliance controls, reporting, and risk management. Each layer affects the client experience and determines whether the desk can scale beyond manual execution.

At an early stage, some firms try to manage OTC trading through chats, spreadsheets, exchange accounts, and manual settlement instructions. This may work for a limited number of trusted clients, but it becomes difficult to control as volumes grow. Pricing becomes harder to standardize, operational errors become more likely, and reporting becomes fragmented.

Institutional clients also expect a more reliable setup, especially when they are trading larger sizes or using the desk as part of their own client-facing service.

A proper OTC desk should be designed as an operating model. Before launch, firms need to define who they serve, how prices are sourced, how trades are executed, where assets are held, how settlement is completed, and how risks are monitored.

Liquidity access

Liquidity is the foundation of an OTC desk. Without reliable liquidity, the desk cannot provide competitive quotes, support larger trade sizes, or maintain consistent execution quality across market conditions.

Firms can source liquidity through direct relationships with market makers, liquidity providers, exchanges, or institutional trading networks. The key question is not only how many liquidity sources are connected, but whether they can provide firm pricing, sufficient depth, fast response times, and stable service during volatile periods.

Price discovery and RFQ workflows

Most OTC desks rely on a request-for-quote model, where the client asks for a price on a specific asset, size, and trading pair. The desk then sources or generates a quote and executes the trade once the client accepts it.

This process needs clear rules. The desk must define how long quotes remain valid, whether prices are firm or indicative, how rejected or expired quotes are handled, and how execution is recorded. These details are important because they shape client trust and protect the desk from unnecessary operational disputes.

Trading infrastructure

The trading layer determines how the desk manages quotes, orders, execution, permissions, and reporting. For a small operation, this may begin with manual tools. For an institutional OTC desk, it usually requires a dedicated platform with a client interface, internal dealer tools, API connectivity, trade history, user roles, and audit trails.

As the desk adds clients, assets, and liquidity sources, it needs to process more requests without creating bottlenecks for traders, operations, or compliance teams.

Settlement and custody workflows

Execution is only one part of OTC trading. Once the trade is agreed, the desk needs to move assets and funds according to the agreed settlement process. This may involve crypto wallets, bank transfers, custodians, settlement partners, or internal treasury accounts.

The desk needs to know when clients must deliver funds, when assets are released, how failed settlement is handled, and who approves each step. Poorly defined settlement processes can create delays, credit exposure, and client dissatisfaction.

Risk management

An OTC desk takes on several types of risk, including market risk, counterparty risk, settlement risk, operational risk, and technology risk. These risks increase as trade sizes grow or as the desk serves more complex clients.

Risk controls may include trade limits, counterparty limits, exposure monitoring, pre-funding rules, approval workflows, and post-trade reconciliation procedures. The goal is not to remove risk completely, but to make sure the desk knows where risk sits and how it is controlled.

Compliance and client onboarding

Before serving clients, an OTC desk needs a clear compliance framework. This includes KYC and KYB checks, AML screening, sanctions controls, transaction monitoring, jurisdictional restrictions, and internal record-keeping.

Compliance should not be treated as a separate step after launch. It affects who the desk can serve, which assets and pairs it can offer, how transactions are monitored, and what information must be collected before execution. For institutional clients, strong onboarding and compliance processes are part of the product experience.

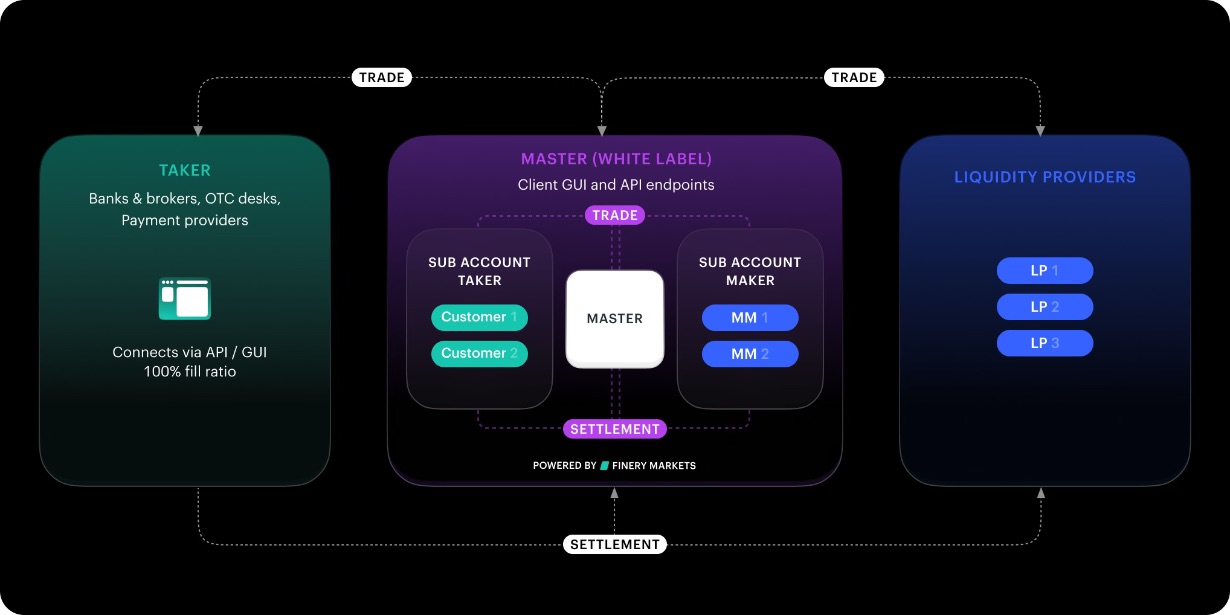

Control vs Speed: White Label Crypto OTC Desk

Once the business case is clear, the next decision is how to launch the OTC desk itself. In practice, firms usually face two options: build the trading infrastructure internally or use white-label OTC desk infrastructure from a specialized provider. Both models can work, but they lead to very different timelines, cost structures, and operational responsibilities.

Building internally gives a firm more control over product design, client workflows, integrations, and long-term roadmap. This can be attractive for companies with large technology teams, established liquidity relationships, and enough time to develop, test, and maintain their own execution stack. However, it also means taking responsibility for every layer of the OTC desk: trading interface, pricing engine, liquidity connectivity, user permissions, reporting, uptime, security, compliance integrations, and ongoing product support.

For many businesses, the bigger challenge is not launching a basic interface, but building the infrastructure required to operate reliably at institutional scale. OTC trading depends on execution quality, speed, price consistency, settlement discipline, and operational control. If these elements are not in place, the desk may struggle to serve larger clients even if demand exists.

White-label OTC desk infrastructure offers a different path. Instead of building the full technology stack from scratch, a company can launch a branded trading environment on top of existing institutional infrastructure. This allows the firm to keep ownership of its client relationships and commercial strategy while relying on a proven technlogy for execution, liquidity access, reporting, and operational workflows.

Building an OTC desk from scratch

Building from scratch may be the right choice for firms that want complete ownership of the technology layer and have the internal resources to support it. This route can offer flexibility, but it usually requires significant investment before the desk can generate meaningful revenue.

Key requirements include:

-

developing the trading interface and internal dealer tools;

-

connecting to liquidity providers and market makers;

-

building pricing, RFQ, and execution logic;

-

setting up reporting, reconciliation, and audit trails;

-

integrating compliance, custody, and settlement workflows;

-

maintaining infrastructure, security, and uptime;

-

staffing technology, product, trading, operations, and support teams.

The main risk is time to market. While the firm is building, competitors may already be serving the same client demand. Internal development can also become more complex as the desk adds more assets, pairs, clients, and liquidity relationships.

Launching with a white-label OTC desk

A white-label OTC platform allows a firm to launch a crypto trading service under its own brand without developing the core infrastructure internally. The provider supplies the execution technology, platform architecture, and often access to an existing liquidity network, while the client-facing company manages its own market positioning, customer relationships, and commercial model.

This model is especially relevant for brokers, payment providers, fintech companies, banks, EMIs, and crypto businesses that already have a client base but do not want to spend years and millions building an institutional trading stack. Instead of starting with infrastructure development, they can focus on distribution, onboarding, client service, and revenue growth.

A white-label model can also reduce operational complexity. The firm still needs clear compliance, settlement, and risk processes, but it does not need to build every technical component itself. This can make the launch process faster, more predictable, and easier to scale.

The key trade-off: speed vs control

The choice between building and using white-label infrastructure is not simply a question of cost. It is a strategic decision about where the firm wants to create value.

Building from scratch gives more control, but also increases development time, operational responsibility, and maintenance burden. White-label infrastructure reduces the technical load and can accelerate launch, but it requires choosing a provider whose technology, liquidity access, and operating model match the firm’s institutional standards.

For most companies entering the OTC market, the goal is not to avoid complexity entirely. It is to place complexity in the right layer. Client relationships, positioning, pricing strategy, and market expansion can remain with the business, while the execution infrastructure is supported by a specialized technology provider.

Step-by-step: how to launch an OTC desk

Launching an OTC desk requires a structured sequence of decisions. The exact process depends on the company’s business model, target clients, regulatory setup, and existing infrastructure, but the core steps are usually the same: define the commercial model, secure liquidity access, choose the technology layer, set up compliance and settlement workflows, test execution, and launch with a controlled client group.

For firms that build everything internally, each of these steps can become a separate technology and operations project. A white-label model changes the sequence. Instead of starting with years of infrastructure development, companies can build their OTC desk in 24 hours around an existing institutional trading stack and focus more directly on client segmentation, liquidity configuration, branding, onboarding, and revenue model.

This is where solutions such as FM White Label can support the launch process. The platform is designed for businesses that want to offer a branded B2B crypto trading environment while relying on existing infrastructure for execution, liquidity access, risk controls, reporting, and settlement workflows.

Step 1. Define your OTC desk model

Before choosing technology or liquidity providers, the firm needs to define what kind of OTC desk it wants to operate. A broker launching crypto execution for existing clients will have different requirements from a payment provider supporting stablecoin conversion or a fintech building an embedded trading service.

Key questions include:

-

Who are the target clients?

-

Which assets and trading pairs will be offered?

-

Will the desk focus on crypto-to-crypto, fiat-to-crypto, stablecoins, or all of them?

-

Will pricing be manual, automated, or hybrid?

-

Will the desk operate as principal, agent, or through a matched-principal model?

Step 2. Choose your liquidity model

Liquidity determines the desk’s ability to offer competitive prices and execute client demand. Firms can work with a single liquidity provider, connect to several market makers, or use a platform that aggregates access to multiple institutional counterparties.

A single-provider model may be easier to launch, but it can create dependency on one source of pricing and availability. A multi-provider model can improve price discovery and resilience, but it also requires connectivity, relationship management, and operational controls. Aggregated liquidity can reduce some of this complexity by allowing the desk to access a broader network through one infrastructure layer.

For example, Finery Markets’ OEMS with aggregated order book brings together liquidity from multiple providers into a single view, helping firms compare available prices and depth across connected counterparties. For companies launching an OTC desk through a white-label model, this type of infrastructure can make liquidity access easier to manage without requiring the business to build and maintain every provider connection independently.

Step 3. Select the right white-label OTC desk technology

The technology layer should support the way the desk wants to serve clients. At minimum, it should allow the team to manage quotes, execute trades, maintain client records, control user permissions, and generate reports. For more advanced use cases, API connectivity, RFQ workflows, quote streams, position management, and integration with custody or compliance tools may be required.

With a white-label model, the question is not only whether the platform can support trading. It is whether the firm can operate the desk under its own brand, configure access for different client types, apply markups, manage risk limits, and give clients a professional trading experience without building the full infrastructure internally.

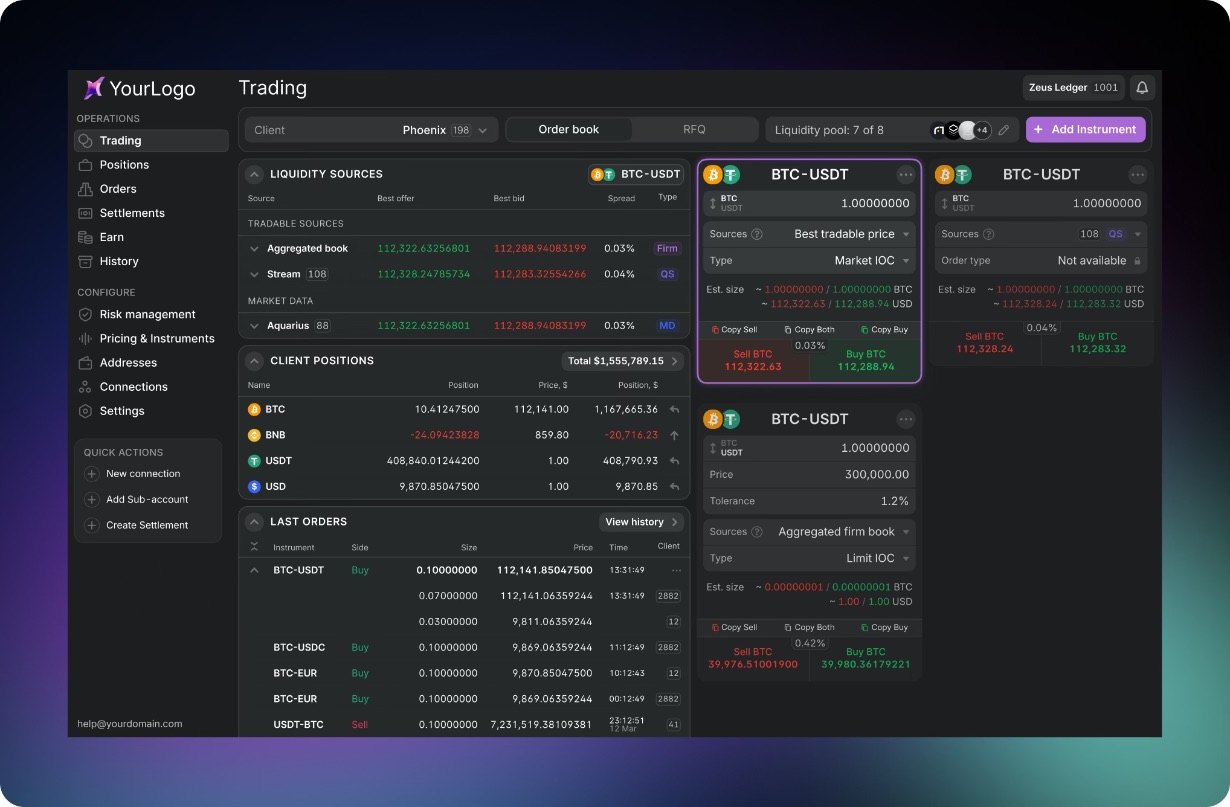

This is where FM White Label brings a more complete value proposition for companies launching an OTC desk. The solution combines a branded client-facing GUI, custom API endpoints via WebSocket, REST, and FIX 4.4, and a white-labeled demo environment that can be used before going live with clients. It also supports multi-role account access, allowing firms to create, modify, and remove accounts while managing permissions across trading, risk, settlement, API, and user administration functions.

For OTC desk operators, the master and sub-account structure is especially important. A firm can use a master account to manage liquidity access, client sub-accounts, risk parameters, markups, positions, and settlement flows from one environment. Each sub-account can have its own tradable order book based on the master liquidity pool, credit lines, risk limits, and spread management settings. This makes the infrastructure relevant not only for reselling external liquidity, but also for segmenting client groups, separating business lines, internalizing customer flow, or creating access points for different types of institutional clients.

Scalability also depends on the quality of the underlying infrastructure. FM White Label is built on AWS-based infrastructure with 99.99% uptime, a sub-1 millisecond proprietary matching engine, pre-trade risk controls, and capacity to process more than 2 million orders per minute. For companies planning to launch and scale a white-label OTC desk, these features help reduce the need for in-house development while supporting execution, reporting, risk management, and settlement workflows from the start.

Step 4. Configure branding, client access, and account structure

A white-label OTC desk should not feel like a third-party product pushed onto clients. It should operate as part of the company’s own service offering. That means configuring the branded client interface, API endpoints, access rights, user roles, and account structure before launch.

For example, a firm may need separate sub-accounts for different clients, business lines, geographies, or liquidity relationships. Each account may require its own permissions, trading limits, settlement setup, reporting access, and markup logic. This structure allows the business to serve multiple client groups through one platform while keeping operational control at the master-account level.

This step is important because it connects the commercial model with the actual client experience. The way accounts are structured will affect onboarding, trading permissions, pricing, reporting, risk management, and settlement.

Step 5. Set up compliance, onboarding, and legal processes

An OTC desk needs to know who it can serve before it starts trading. This requires client onboarding processes, KYC and KYB checks, AML screening, sanctions controls, jurisdictional rules, and internal approval workflows. For institutional clients, onboarding also includes collecting corporate documentation, beneficial ownership information, trading authorizations, and settlement instructions.

Legal documentation should define the commercial relationship between the desk and its clients. This may include trading terms, settlement obligations, risk disclosures, service agreements, fee schedules, and rules for failed or delayed settlement.

White-label infrastructure can support the operating model, but it does not replace the firm’s own compliance responsibilities. The desk still needs to define who its clients are, which jurisdictions it serves, which assets it offers, and what internal approvals are required before trading starts.

Step 6. Configure settlement and custody workflows

Settlement is one of the most important parts of the OTC operating model. The desk needs to define how fiat, stablecoins, and digital assets move before and after execution. This includes wallet setup, bank account flows, custodian relationships, transaction approvals, reconciliation, and confirmation procedures.

The desk also needs to decide whether clients must pre-fund trades, whether settlement is handled after execution, and how exposure is controlled between trade agreement and final settlement. These choices affect both client experience and risk management.

Settlement workflows should be configured alongside trading permissions and account structure. The goal is to make the post-trade process as controlled as the execution process: clear instructions, verified counterparties, auditable activity, and reliable reporting.

Step 7. Test execution, reporting, and operational controls

Before opening the desk to a broader client base, firms should test the full workflow from quote request to final settlement. This includes RFQ handling, price acceptance, trade booking, confirmations, reporting, reconciliation, and exception management.

Testing should cover normal trading conditions and edge cases. For example, what happens if a quote expires, a client sends funds late, a liquidity provider rejects a trade, or a transaction requires additional compliance review? These scenarios should be addressed before they occur in production.

For a white-label launch, this stage should also include testing the branded environment, client permissions, API connections, markup settings, risk limits, reports, and settlement instructions. A test environment can help teams validate the workflow before going live with real client activity.

Step 8. Launch with selected clients before scaling

A controlled launch is usually better than a broad public rollout. Starting with a small group of trusted clients allows the desk to validate pricing, execution, reporting, settlement, and support processes under real market conditions.

This phase also helps the firm understand what clients actually need. Some may require API access, others may need additional reporting, broader asset coverage, faster settlement, or different quote workflows. These insights can guide the next stage of product development.

Once the desk has stable workflows and client feedback, it can expand liquidity coverage, onboard more clients, add new pairs, and scale trading volumes with more confidence. With a white-label model, the business can focus this scaling phase on distribution, client service, and commercial growth rather than rebuilding the core trading infrastructure.

Key features of a white-label OTC desk platform

A white-label OTC desk platform should do more than provide a branded login page. For institutional clients, the quality of the trading experience depends on what sits behind the interface: liquidity access, execution logic, account structure, risk controls, reporting, and settlement workflows. The goal is to give the business a ready infrastructure layer while allowing it to operate the service under its own brand.

The right platform should support both the client-facing experience and the internal operating model. Clients need a reliable environment to request prices, place orders, monitor trades, and access reporting. The desk operator needs tools to manage liquidity, pricing, permissions, markups, exposure, and post-trade processes.

Branded client-facing environment

A white-label OTC desk should allow the business to offer crypto trading under its own brand. This includes a branded trading interface, custom access points, and a client experience that feels consistent with the company’s existing product ecosystem.

For brokers, payment providers, fintechs, and institutional service providers, this matters commercially. The client relationship remains with the business launching the desk, while the underlying execution infrastructure is provided by a specialized technology partner.

Access to institutional liquidity

Liquidity access is one of the main reasons firms choose a white-label model. Instead of building and maintaining individual connections to multiple liquidity providers from the start, the desk can operate through infrastructure that already supports institutional liquidity access.

A strong platform should help the operator source competitive prices, manage available depth, and support execution across the assets and pairs required by its clients. For OTC desks serving larger or more active clients, liquidity quality should be evaluated not only by spread, but also by quote reliability, market depth, uptime, and settlement conditions.

Flexible account and permission management

Institutional OTC businesses often need to support multiple client types, internal teams, business lines, and geographies. This requires more than a single administrator account. The platform should allow the operator to create and manage sub-accounts, assign roles, set permissions, and control access to trading, risk, settlement, reporting, and API functions.

This structure is especially important for firms that want to segment client groups, operate different liquidity pools, apply different markups, or manage separate trading conditions for different institutional clients.

Pricing, markups, and risk controls

A white-label OTC desk needs commercial flexibility. The operator should be able to define how prices are shown to clients, how spreads or markups are applied, and how risk parameters are managed across accounts.

Pre-trade risk controls, credit limits, exposure monitoring, and account-level settings help the desk operate with greater discipline. These tools are important because OTC trading often involves larger order sizes, settlement timing differences, and more complex counterparty relationships than standard retail exchange trading.

API connectivity

Many institutional clients do not want to trade only through a graphical interface. Brokers, payment companies, fintechs, and trading firms may need API connectivity to embed OTC execution into their own systems, automate workflows, or serve downstream clients.

A white-label OTC platform should therefore support robust API access, including market data, order placement, trade history, and reporting. For more advanced institutional use cases, FIX connectivity can be important because it allows crypto trading infrastructure to fit into existing capital markets workflows.

Reporting, audit trails, and operational transparency

Reporting is not an afterthought for an OTC desk. Clients need trade confirmations, histories, and clear records. Operators need visibility into volumes, pricing, client activity, exposures, and settlement status.

A strong white-label platform should support reporting and audit trails that make operations easier to monitor and reconcile. This becomes increasingly important as the desk scales, adds more clients, and handles more complex liquidity and settlement workflows.

Settlement workflow support

Execution quality matters, but the client experience is not complete until settlement is completed correctly. The platform should support clear post-trade workflows, settlement instructions, account-level controls, and reconciliation processes.

For firms launching an OTC desk, this can reduce operational friction. Instead of managing execution and settlement as disconnected processes, the desk can operate them within a more controlled infrastructure setup.

Scalable infrastructure

A white-label OTC desk should be able to support growth without forcing the operator to rebuild its core systems. As the business adds clients, assets, trading pairs, liquidity providers, and integrations, the platform must remain stable and responsive.

Scalability is especially relevant for firms that expect OTC trading to become a strategic business line rather than a small add-on product. The infrastructure needs to support higher volumes, more complex account structures, and growing institutional expectations around uptime, latency, and operational resilience.

Common mistakes when launching an OTC desk

Launching an OTC desk can look straightforward from the outside: connect to liquidity, quote clients, execute trades, and manage settlement. In practice, most challenges appear in the details. If pricing, execution, risk, compliance, and post-trade workflows are not designed properly from the beginning, the business may struggle to scale even when client demand is strong.

Treating liquidity as a commodity

Not all liquidity is equal. Providers may differ in spread, depth, response time, rejection rates, uptime, settlement terms, and performance during volatility. OTC desk operators should evaluate liquidity by execution quality, reliability, and operational fit — not only by the displayed price.

Relying too heavily on manual workflows

Chats, spreadsheets, screenshots, and email confirmations may work at a very early stage, but they become fragile as volumes grow. Manual workflows make it harder to control pricing, track approvals, reconcile trades, monitor exposure, and maintain clean records.

Underestimating settlement complexity

Execution is only half of the trade. The desk still needs to receive funds, deliver assets, confirm settlement, reconcile balances, and handle exceptions. Before launch, firms should define how fiat, stablecoins, and digital assets move between clients, liquidity providers, custodians, and internal accounts.

Launching without clear client segmentation

Different clients use OTC desks for different reasons. Brokers may need APIs and downstream reporting, payment providers may need stablecoin liquidity and fast conversion, while banks or EMIs may require stronger governance and documentation. Segmentation should influence asset coverage, pricing, limits, settlement terms, reporting, and support.

Choosing technology that cannot scale

A basic trading interface may be enough to demonstrate demand, but not enough to operate an institutional OTC desk over time. Common limitations include weak API access, poor permission management, limited account structure, no markup controls, insufficient risk settings, or difficulty integrating with custody and compliance workflows.

Ignoring compliance until after launch

Compliance should be part of the OTC desk design from day one. The desk needs to know which clients it can onboard, which jurisdictions it can serve, which assets and pairs it can offer, and what monitoring or reporting obligations apply to its business model.

Treating white label as only a shortcut

White-label OTC infrastructure can accelerate launch, but it does not replace strategic decisions. The firm still needs to define its business model, client segments, pricing approach, risk appetite, legal framework, and operating procedures. The strongest model combines client ownership and market positioning with infrastructure built for institutional execution, liquidity access, reporting, and operational control.

How Finery Markets helps businesses launch OTC desks

Finery Markets supports businesses that want to launch institutional crypto trading services without building the full OTC infrastructure from scratch.

Through FM White Label, companies can offer a branded B2B trading environment while relying on Finery Markets’ technology stack for execution, liquidity access, account management, risk controls, reporting, and settlement workflows.

This model is designed for firms that already have client relationships or a clear distribution channel, but need the infrastructure layer to turn OTC trading into a scalable service. Brokers, payment providers, fintech companies, banks, EMIs, OTC desks, and digital asset businesses can use white-label infrastructure to bring crypto liquidity to their clients under their own brand.

Launch under your own brand

FM White Label allows companies to provide a branded trading experience through a client-facing GUI and custom API endpoints. The business keeps the client relationship, pricing strategy, and commercial positioning under its own name, while Finery Markets supports the execution layer behind it.

Access institutional liquidity through one infrastructure layer

Liquidity is one of the hardest parts of launching an OTC desk independently. Finery Markets helps simplify this through institutional liquidity access and aggregated liquidity infrastructure, allowing firms to operate through a single platform instead of building every provider connection separately.

Manage clients, sub-accounts, markups, and risk controls

FM White Label uses a master and sub-account structure, which is particularly relevant for OTC desk operators. A firm can manage client accounts, configure access rights, apply markups, set risk limits, and monitor positions from one environment. This helps brokers, payment providers, and OTC desks serve different client groups or business lines with greater control.

Support both GUI and API-driven trading

Different clients require different workflows. Some prefer a graphical interface for RFQ-style execution and trade monitoring, while others need API connectivity to embed trading into internal systems or serve downstream clients. FM White Label supports both approaches through a branded GUI and custom API endpoints, including WebSocket, REST, and FIX 4.4 connectivity.

It also gives OTC desk operators access to Finery Markets’ hybrid trading model, which combines order-driven and quote-driven execution. Clients can interact with firm liquidity in the order book or request quotes from multiple liquidity providers through RFQ, then choose the execution method that best fits the trade size, asset liquidity, and market conditions. This is especially relevant for OTC desks that need both transparent price discovery and the ability to handle larger or less liquid trades with reduced market impact.

Build on infrastructure designed for institutional scale

A white-label OTC desk needs to be reliable from the start. Finery Markets’ infrastructure is built for institutional trading, with AWS-based deployment, 99.99% uptime, a proprietary matching engine, pre-trade risk controls, and capacity to process high order volumes. For companies launching an OTC desk, this reduces the need to build and maintain critical trading infrastructure internally.

How long does it take to launch an OTC desk?

The answer depends on whether the firm builds the OTC desk internally or uses existing white-label infrastructure. Building from scratch can take months or longer, especially if the business needs to develop the trading interface, connect liquidity providers, build pricing and execution logic, configure reporting, integrate compliance workflows, and test settlement operations.

With a white-label model, the timeline can be much shorter. With FM White Label, clients can typically have a full setup in around a week, depending on the required configuration, branding, liquidity model, account structure, and internal approval process. This makes the white-label route especially relevant for firms that already have client demand and want to bring an OTC trading service to market without waiting for a long internal development cycle.

The important distinction is between technical setup and full operational readiness. A branded environment can be configured quickly, but the company still needs to complete its own legal, compliance, onboarding, settlement, and internal governance steps before serving clients in production.

In practice, this means that white-label infrastructure can compress the technology timeline from months to days, while the final go-live date will depend on how prepared the firm is from a business, legal, and operational standpoint.

The bottom line

Launching an OTC desk in 2026 requires a clear view of the market opportunity and the operational model behind it. Institutional demand for crypto, fiat, and stablecoin liquidity continues to grow, but clients expect more than access to prices. They need reliable execution, transparent workflows, strong controls, and a service that can support larger and more complex trading activity.

White-label OTC infrastructure can shorten the path to market while keeping the core client relationship under the company’s own brand. The strongest setups will combine speed, liquidity access, trading technology, risk management, reporting, and settlement discipline into one scalable OTC offering.

FAQ: launching a crypto OTC desk

How do I launch an OTC desk?

To launch an OTC desk, a firm needs to define its target clients, choose a liquidity model, select the trading infrastructure, set up compliance and onboarding processes, configure settlement workflows, and test execution before going live. Companies can either build the infrastructure internally or use white-label OTC desk technology to shorten the launch timeline.

What is a white-label OTC desk?

A white-label OTC desk is a branded crypto trading service operated by one company on top of infrastructure provided by a technology partner. The company keeps its own brand, client relationships, pricing strategy, and commercial model, while the provider supports the trading platform, liquidity access, account structure, risk controls, reporting, and settlement workflows.

Can I launch an OTC desk without building technology from scratch?

Yes. A firm can use white-label OTC desk infrastructure instead of building the trading stack internally. This allows the business to launch a branded OTC trading service faster, while focusing on clients, onboarding, compliance, and revenue growth rather than developing the full execution infrastructure.

How much does it cost to launch a crypto OTC desk?

The cost depends on the launch model. Building from scratch usually requires investment in development, infrastructure, liquidity connectivity, compliance integrations, security, product support, and internal teams. A white-label model can reduce upfront technology costs because the core trading infrastructure is already provided, although firms still need to account for compliance, legal, settlement, operations, and go-to-market costs.

How long does it take to launch an OTC desk?

Building an OTC desk internally can take months or longer. With white-label infrastructure, the timeline can be significantly shorter. With FM White Label, clients can typically have a full setup in around a week, depending on the required configuration, branding, liquidity model, account structure, and internal approvals.

Who needs an OTC desk?

OTC desks are relevant for brokers, payment providers, fintech companies, banks, EMIs, stablecoin businesses, crypto companies, family offices, hedge funds, and institutional trading firms. Any business serving clients that need reliable access to crypto, fiat, or stablecoin liquidity may consider launching an OTC desk.

.png)