Stablecoins are increasingly being used as settlement infrastructure for cross-border payments. Instead of relying only on correspondent banks, payment companies, fintechs, OTC desks, and digital asset businesses can use stablecoins to move value across borders faster and with fewer intermediaries.

One of the most common models behind this shift is known as a stablecoin sandwich. In simple terms, it means converting fiat currency into a stablecoin, transferring that stablecoin over blockchain rails, and then converting it back into fiat currency in the recipient’s market.

The model is especially relevant for businesses that still operate in fiat currencies but want to benefit from blockchain-based settlement. The stablecoin sits “in the middle” of the transaction, while the sender and recipient remain connected to local currency systems on both sides.

What is a stablecoin sandwich?

A stablecoin sandwich is a cross-border payment flow where fiat currency is converted into a stablecoin, transferred onchain, and then converted back into fiat currency for the recipient.

The basic structure looks like this:

Local fiat currency → stablecoin → local fiat currency

For example, a company in the United States may need to pay a supplier in Mexico. Instead of sending money through a traditional correspondent banking chain, the company or its payment provider converts USD into a dollar-backed stablecoin such as USDC or USDT, transfers it across blockchain rails, and then converts it into Mexican pesos on the other side.

The sender may only see a USD debit, and the recipient may only see an MXN credit. The stablecoin layer can remain invisible to the end users while still serving as the settlement rail in the middle.

Why is it called a “sandwich”?

The term comes from the structure of the payment flow. Fiat currency sits on both ends of the transaction, while the stablecoin is placed in the middle. The stablecoin layer is the “filling” that connects two fiat systems.

This is useful because most businesses still invoice, report, pay taxes, manage payroll, and reconcile accounts in fiat currencies. They may not want to hold crypto assets directly, but they can still use stablecoins as an operational bridge for settlement.

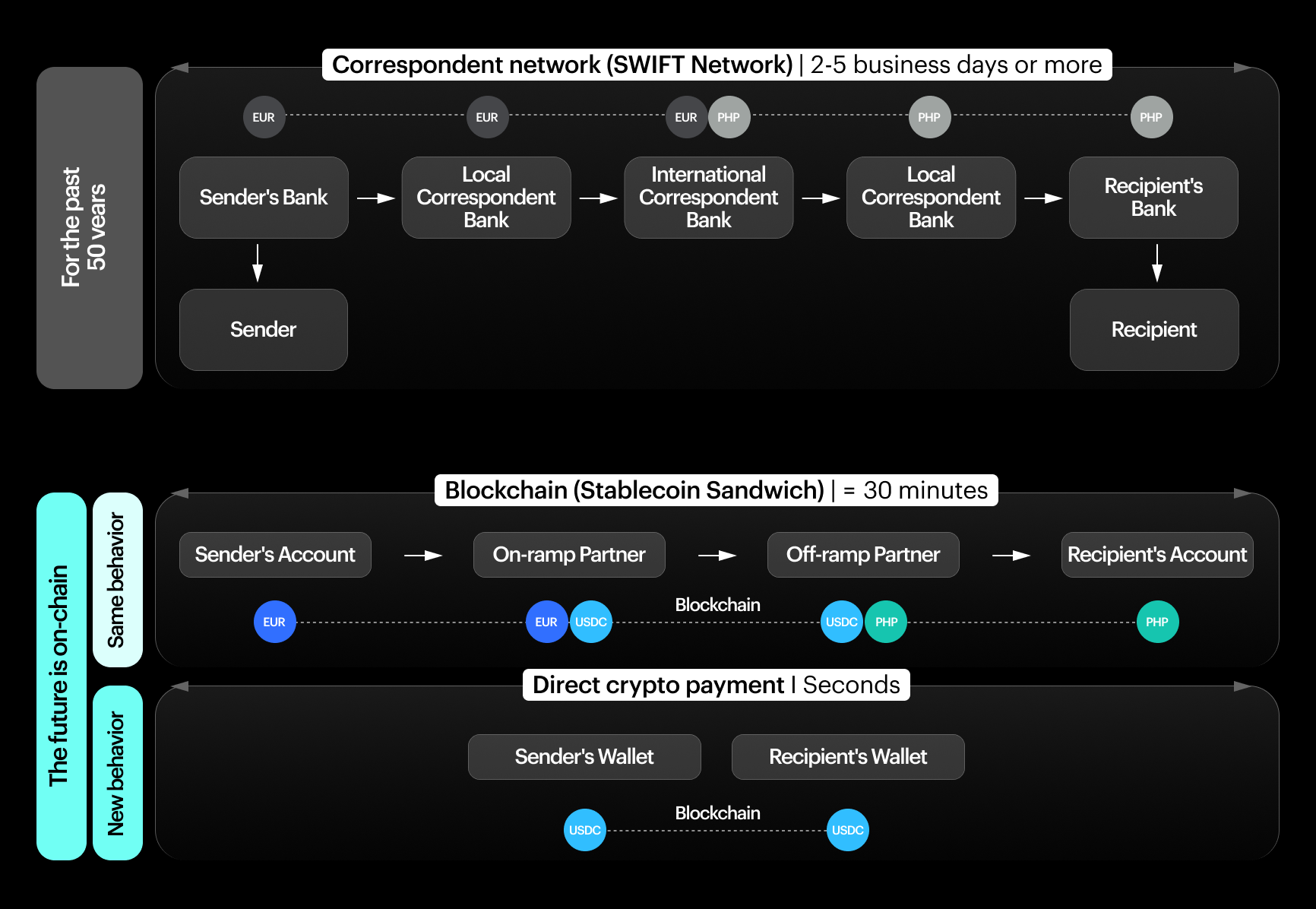

Stablecoin sandwich vs traditional correspondent banking

Traditional cross-border payments often move through a chain of correspondent banks. Each intermediary may add fees, processing time, compliance checks, cut-off times, and FX spreads. This can make international transfers slower, less transparent, and harder to reconcile.

A stablecoin sandwich changes the middle layer of the transaction. Instead of routing value through several banking intermediaries, the payment provider uses stablecoins to transfer value across blockchain infrastructure.

That does not remove every source of friction. Businesses still need fiat on-ramps, off-ramps, compliance controls, liquidity, custody, and reporting. But it can reduce dependence on legacy settlement chains and make cross-border flows faster, more transparent, and easier to automate.

How does a stablecoin sandwich work?

A stablecoin sandwich works by separating the payment journey into three parts: fiat conversion at the origin, stablecoin transfer in the middle, and fiat conversion at the destination.

The user experience can look similar to a regular international payment. The sender starts with local currency, and the recipient receives local currency. The main difference is the settlement layer used between those two points.

In practice, the stablecoin leg is usually handled by a payment provider, fintech platform, OTC desk, exchange, or liquidity partner. These intermediaries manage the conversion, transfer, compliance checks, and payout process needed to make the transaction work.

Step 1: fiat on-ramp

The process begins when the sender converts local currency into a stablecoin.

For example, a business may fund a payment in USD, EUR, GBP, or another local currency. That fiat amount is then exchanged for a stablecoin, usually one pegged to a major currency such as the U.S. dollar or euro.

This conversion can happen through different types of providers, including:

-

crypto exchanges

-

OTC desks

-

payment companies

-

licensed money transmitters

-

banking or fintech partners

-

institutional liquidity providers

This first step is important because it determines the initial execution cost. The quoted rate, FX spread, stablecoin liquidity, transaction size, and provider fees all affect the final economics of the payment.

Step 2: onchain stablecoin transfer

Once the fiat currency has been converted into a stablecoin, the stablecoin is transferred over blockchain rails.

This is the part of the process where stablecoins can offer a clear operational advantage. Blockchain networks can settle transactions outside traditional banking hours, including nights, weekends, and holidays. Depending on the network, the transfer itself can be completed in seconds or minutes.

However, the blockchain transfer is only one part of the full payment journey. A fast onchain transaction does not automatically mean the recipient receives fiat instantly. The final speed still depends on compliance screening, liquidity availability, local payment rails, and the efficiency of the off-ramp.

Step 3: fiat off-ramp

At the destination, the stablecoin is converted into the recipient’s local currency.

For example, a payment provider may receive USDC and convert it into Brazilian reals, euros, British pounds, or another fiat currency before sending funds to the recipient’s bank account or local wallet.

This off-ramp stage is often where the biggest operational complexity appears. The provider needs enough local currency liquidity, reliable banking access, regulatory coverage, transaction monitoring, and payout infrastructure.

For businesses, this means the quality of a stablecoin sandwich depends heavily on both ends of the transaction. The middle blockchain transfer may be efficient, but the full payment experience is shaped by the strength of the fiat on-ramp and off-ramp.

Example: USD to BRL stablecoin sandwich

A U.S.-based company needs to pay a supplier, contractor, or local partner in Brazil.

In a traditional payment flow, the company may send USD through one or more correspondent banks before the funds are converted into Brazilian reals and delivered to the recipient’s account. This can involve several intermediaries, unclear fees, and delays caused by banking cut-off times.

In a stablecoin sandwich flow, the process may look different:

USD → USDC → onchain transfer → BRL

The sender funds the payment in USD. The payment provider converts USD into USDC, transfers USDC over blockchain rails, and then converts USDC into BRL through a local liquidity partner or payout provider. The recipient receives Brazilian reals, while the stablecoin is used only as the settlement asset between the two fiat currencies.

What happens behind the scenes?

Although the model looks simple, a production-grade stablecoin sandwich requires several operational layers.

The provider may need to manage customer onboarding, KYC, AML checks, sanctions screening, wallet infrastructure, blockchain transaction monitoring, FX conversion, liquidity sourcing, treasury balances, local payouts, and reconciliation records.

For smaller payments, much of this can be automated. For larger institutional flows, the process becomes more execution-sensitive. The provider must secure reliable pricing, minimize slippage, control settlement risk, and ensure that both fiat legs of the transaction are properly funded.

This is why the stablecoin sandwich should not be viewed only as a payment concept. It is also a liquidity and execution workflow. The quality of the result depends on how efficiently value can be converted, transferred, and paid out across all three layers.

Why stablecoin sandwiches emerged in cross-border payments

Stablecoin sandwiches emerged because traditional cross-border payment infrastructure was not designed for today’s speed of global business.

Many companies now operate across multiple jurisdictions, pay suppliers and contractors internationally, manage treasury balances across regions, and serve customers in markets where local banking rails may be slower or more expensive. Yet the underlying payment stack often still depends on correspondent banking relationships, banking hours, local cut-off times, and multiple intermediaries.

Stablecoins introduced a new settlement layer into this process. Instead of replacing fiat currencies completely, they can act as a bridge between fiat systems that do not connect efficiently with each other.

Limitations of traditional cross-border payments

Traditional cross-border payments can involve several banks and payment intermediaries before funds reach the recipient.

This creates several common issues:

-

settlement delays

-

intermediary fees

-

opaque FX spreads

-

limited payment tracking

-

banking cut-off times

-

higher rejection risk

-

complex reconciliation

For businesses, these issues are not just operational inconveniences. They affect working capital, supplier relationships, treasury planning, and the ability to move funds quickly between markets.

A payment that takes several days to settle can create liquidity pressure. A transfer with unclear fees can complicate accounting. A delayed payout can affect a contractor, merchant, or supplier who depends on predictable cash flow.

Why stablecoins became useful payment rails

Stablecoins became useful because they allow value to move on blockchain networks without the same dependency on traditional banking schedules.

A stablecoin transfer can take place 24/7, including weekends and holidays. It can be tracked onchain. It can also be integrated into programmable workflows through APIs, wallets, and automated treasury systems.

For payment providers and institutional businesses, this creates a practical advantage: stablecoins can serve as a settlement asset between counterparties, platforms, or regions without forcing the end user to interact directly with crypto.

This is one reason the stablecoin sandwich model is so important. It lets businesses use stablecoin rails while still maintaining fiat-based user experiences.

Why businesses still need fiat at both ends

Despite the growth of stablecoins, most companies still operate primarily in fiat currencies.

They invoice customers in local currency, pay suppliers in local currency, report financial results in fiat, calculate taxes in fiat, and reconcile accounts through traditional finance systems. Employees, vendors, merchants, and regulators usually expect fiat-denominated records and payments.

This is why the stablecoin sandwich is often more practical than a fully crypto-native payment flow. It does not require both sides of the transaction to hold stablecoins or manage wallets directly.

The sender can pay in one fiat currency. The recipient can receive another fiat currency. The stablecoin sits in the middle as the settlement layer, helping move value between markets while keeping the business workflow familiar on both sides.

Stablecoin sandwich vs other stablecoin payment models

The stablecoin sandwich is one of several models used in stablecoin-based payments. The right structure depends on who sends the funds, who receives them, whether each side wants fiat or stablecoins, and how much liquidity is available in the relevant corridor.

For businesses, the key question is not only whether stablecoins are involved. It is where the fiat conversion happens, who manages the stablecoin leg, and whether the recipient ultimately receives fiat or digital assets.

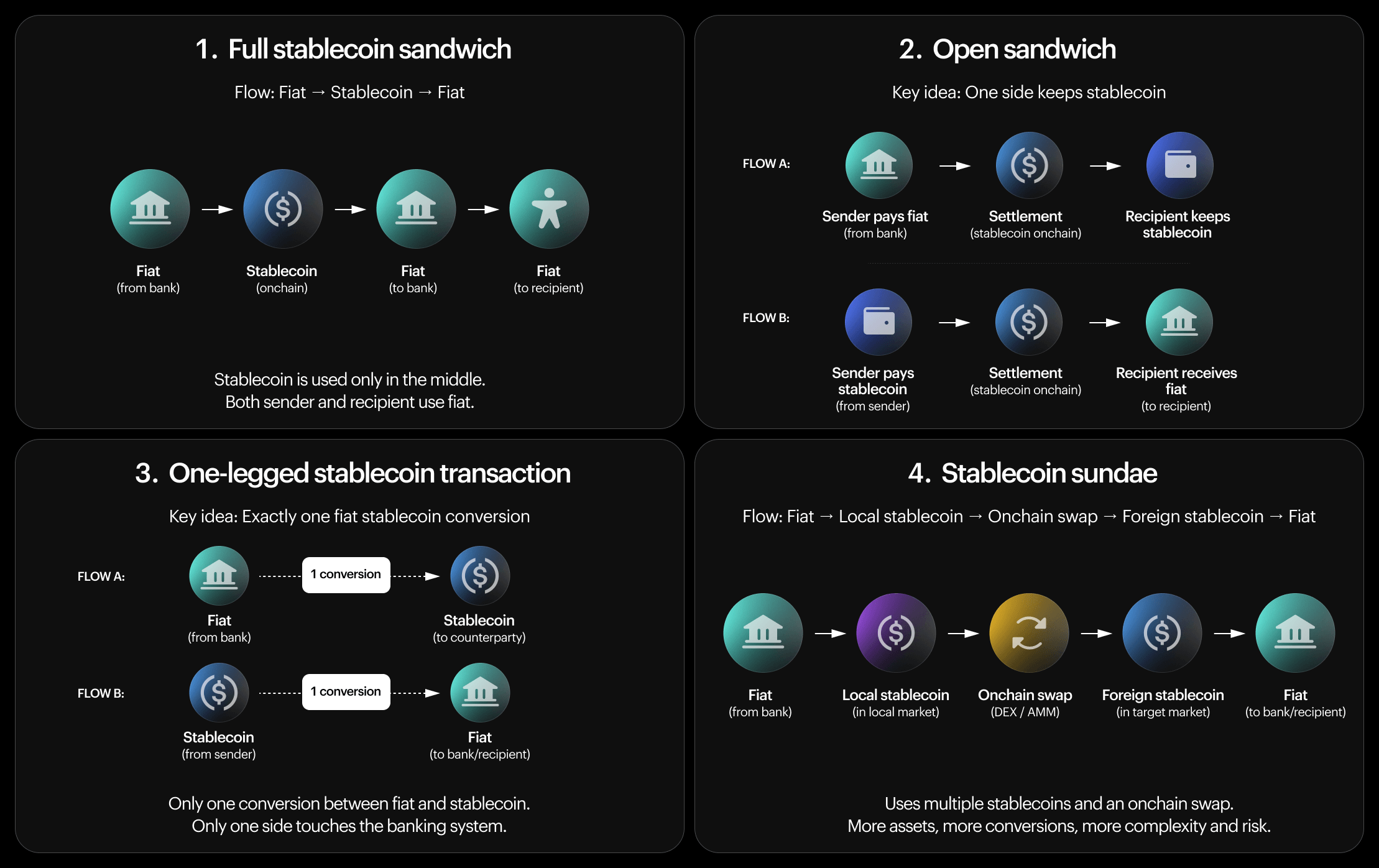

Full stablecoin sandwich

A full stablecoin sandwich follows the basic model:

Fiat → stablecoin → fiat

This is the most common structure for businesses that want to use blockchain rails without changing the user experience at either end of the transaction.

The sender pays in fiat. The recipient receives fiat. The stablecoin is used as a backend settlement asset in the middle.

This model can be useful for payment companies, remittance providers, fintech platforms, marketplaces, and institutional businesses that need faster settlement but still operate through local currency systems.

Open sandwich

An open sandwich keeps one side of the transaction in stablecoins. The flow may look like this:

Fiat → stablecoin

or:

Stablecoin → fiat

In the first case, the sender starts with fiat, but the recipient keeps the funds in stablecoins. In the second case, the sender uses stablecoins, while the recipient receives local fiat currency.

This model can work when one party is comfortable holding stablecoins or already uses them for treasury, trading, or settlement. It may also be relevant in markets where stablecoins are used as a dollar-denominated store of value or as a working capital tool.

One-legged stablecoin transaction

A one-legged stablecoin transaction involves only one fiat conversion. It is similar to an open sandwich but often used more broadly to describe flows where only one side of the payment touches the banking system.

For example, a company may convert USD into USDC and send the stablecoin to a counterparty that wants to hold USDC. Alternatively, a crypto-native company may send USDC to a provider that converts it into EUR for a fiat payout.

One-legged flows can be simpler than a full sandwich because there is only one conversion point. But they also require at least one participant to hold, receive, or manage stablecoins directly.

Stablecoin sundae

A stablecoin sundae is a more layered model. Instead of using a single stablecoin in the middle, the payment may move through local or currency-specific stablecoins.

The structure can look like this:

Fiat → local stablecoin → onchain swap → foreign stablecoin → fiat

For example, a sender may convert local fiat into a local-currency stablecoin, swap it onchain into another stablecoin, and then convert that into fiat in the recipient’s market.

This model can be useful if local stablecoins become more liquid and regulated across different markets. However, it adds complexity: more assets, more conversion points, more liquidity requirements, and potentially more smart contract or execution risk.

Which model works best for businesses?

There is no universal best model. The right structure depends on the business case.

A full stablecoin sandwich is often the most practical option when both parties want to stay in fiat. An open sandwich may work better when one side already uses stablecoins. A one-legged transaction can be efficient for crypto-native companies or institutional counterparties. A stablecoin sundae may become more relevant as local stablecoin liquidity develops.

For most businesses, the decision comes down to five factors: corridor coverage, regulatory requirements, liquidity depth, accounting needs, and the quality of the on-ramp and off-ramp. The payment structure only works if the business can convert in and out of stablecoins reliably, at predictable rates, and with the required compliance controls.

Benefits of a stablecoin sandwich

The main benefit of a stablecoin sandwich is that it can make cross-border payments faster, more flexible, and more transparent while keeping fiat currencies on both sides of the transaction.

For businesses, this matters because the stablecoin layer can improve settlement without forcing customers, suppliers, or partners to directly manage digital assets. The sender pays in local currency, the recipient receives local currency, and the blockchain rail operates in the background.

Faster settlement

Stablecoin transfers can settle much faster than traditional cross-border bank payments, especially when funds need to move outside regular banking hours.

In a traditional correspondent banking flow, settlement can be delayed by weekends, holidays, intermediary banks, manual reviews, and local cut-off times. In a stablecoin sandwich, the onchain transfer can happen 24/7.

That said, the total payment speed still depends on the full flow. The blockchain transaction may settle quickly, but the fiat on-ramp, compliance screening, off-ramp liquidity, and local payout method still determine when the recipient actually receives funds.

Lower transaction costs

A stablecoin sandwich can reduce costs by replacing some intermediary banking layers with blockchain-based settlement.

This may lower transfer fees, reduce correspondent banking charges, and improve FX efficiency, especially in corridors where traditional cross-border payments are expensive or slow.

However, costs do not disappear. Businesses still need to account for conversion spreads, provider fees, blockchain network fees, local payout charges, and possible liquidity premiums. The final cost depends on execution quality across the entire transaction.

24/7 payment availability

Stablecoins can move outside the operating hours of traditional banking systems.

This is especially relevant for global companies, crypto-native businesses, payment providers, and trading firms that operate across time zones. A business may need to settle obligations on a weekend, rebalance liquidity overnight, or fund a payout corridor when banks are closed.

A stablecoin sandwich can support these workflows by making the settlement leg available continuously, while fiat payouts can be processed when local rails are available.

Better transparency and tracking

Stablecoin transfers can be tracked onchain, which may improve visibility compared with traditional payment chains.

In correspondent banking, payment status can be difficult to trace because funds may pass through several intermediaries. With stablecoin rails, the transfer itself can be verified on a blockchain, giving providers and treasury teams a clearer record of movement.

For businesses, this can support reconciliation, audit trails, and operational monitoring. The benefit becomes stronger when onchain data is combined with payment references, customer records, and reporting tools from the provider.

Reduced need for prefunded foreign accounts

Stablecoin sandwiches can help reduce dependence on prefunded balances in multiple local markets.

Traditionally, payment companies and international businesses may need to hold capital in foreign bank accounts to support local payouts. This can tie up working capital and create treasury inefficiencies.

With stablecoin-based settlement, businesses may be able to move funds into a corridor closer to the time of payment, depending on local liquidity and payout infrastructure. This can improve capital efficiency, although it does not remove the need for liquidity planning entirely.

Better reach in underserved corridors

Stablecoin sandwiches can be useful in corridors where traditional banking access is limited, slow, or expensive.

In some markets, international transfers may involve high fees, long settlement times, or limited correspondent banking coverage. Stablecoins can provide an alternative settlement layer that connects local payment providers, liquidity partners, and digital asset infrastructure.

This does not mean stablecoins solve every corridor problem. Local regulation, banking access, liquidity depth, and payout options still matter. But in selected corridors, the stablecoin sandwich can offer a more flexible way to connect fiat systems that are otherwise inefficiently linked.

Where the friction remains

A stablecoin sandwich can improve cross-border settlement, but it does not remove every bottleneck in the payment chain.

The fastest part of the transaction is often the onchain stablecoin transfer. The more complex parts sit around it: fiat conversion, local payouts, liquidity sourcing, compliance checks, and treasury operations. This is why businesses should evaluate the full payment lifecycle, not only the blockchain leg.

On-ramp and off-ramp bottlenecks

A stablecoin sandwich depends on reliable access to fiat at both ends of the transaction.

The sender’s currency must be converted into a stablecoin, and the stablecoin must later be converted into the recipient’s local currency. If either conversion point is slow, expensive, or operationally weak, the overall payment flow can suffer.

Off-ramps are especially important. A stablecoin can arrive onchain within minutes, but the recipient still needs local fiat delivery through bank transfer, instant payment rails, mobile money, or another payout method. If local rails are unavailable, delayed, or poorly integrated, the final user experience may still feel slow.

Liquidity gaps in local currencies

The stablecoin sandwich works best when there is deep liquidity between the relevant fiat currencies and stablecoins.

In major markets, converting USD into USDC or USDT can be relatively efficient. The challenge often appears in local currency pairs, especially in emerging markets or less liquid corridors.

For example, the cost of a USD → USDC → BRL transaction depends not only on the blockchain transfer, but also on the availability of reliable USDC/BRL liquidity. If liquidity is thin, the provider may need to widen spreads, split orders, delay execution, or rely on prefunded balances.

FX spread and execution risk

A stablecoin sandwich is still exposed to execution quality.

Even when a stablecoin is pegged to a fiat currency, the business still needs to convert between fiat and stablecoin at both ends. Each conversion may include a spread, fee, or price movement risk.

For small payments, this may be manageable. For larger transactions, execution quality becomes more important. Poor pricing, slippage, or insufficient liquidity can reduce the cost advantage of using stablecoin rails.

This is why institutional users often need access to firm, executable pricing rather than indicative rates. The payment may be operationally fast, but the economics still depend on how the conversions are priced and settled.

Network fees and blockchain selection

Blockchain costs vary depending on the network used, transaction size, congestion, and token standard.

Some networks offer very low transaction fees, while others can become expensive during periods of high demand. Businesses also need to consider confirmation times, network reliability, ecosystem support, wallet compatibility, and stablecoin availability.

The cheapest network is not always the best option. For institutional flows, security, liquidity, counterparty support, and operational reliability may matter more than the lowest transaction fee.

Reconciliation and operational complexity

Stablecoin sandwiches introduce new operational requirements for finance and treasury teams.

Businesses need to connect fiat payment records with onchain transaction hashes, wallet movements, conversion rates, fees, payout confirmations, and compliance records. Without proper reporting infrastructure, the process can become difficult to reconcile at scale.

This is especially relevant for companies processing high transaction volumes or operating across multiple countries. They need clear payment references, audit trails, API integrations, accounting exports, and internal controls for who can initiate, approve, and monitor transactions.

Key risks and challenges of a stablecoin sandwich

A stablecoin sandwich can improve cross-border payment flows, but it also introduces risks across fiat conversion, stablecoin selection, custody, compliance, liquidity, payout, and reporting. For institutional users, the model only works if the operational and regulatory setup is as strong as the payment logic.

Regulatory uncertainty

Stablecoin rules are still developing and vary by jurisdiction. A flow that works in one market may require additional licenses, disclosures, reporting, or transaction controls in another.

Businesses should evaluate the model corridor by corridor, including the legal status of the stablecoin, the provider’s licensing position, and the treatment of fiat on-ramps and off-ramps.

AML, KYC, and sanctions screening

Stablecoin payments still require customer verification, wallet screening, transaction monitoring, and sanctions checks.

The blockchain layer can improve transparency, but it does not remove compliance obligations. It adds more data that must be connected to customer records and payment purpose.

Stablecoin issuer risk

Not all stablecoins have the same risk profile. Reserve quality, redemption reliability, transparency, and peg stability all matter.

Even if the stablecoin is held only briefly, it still represents settlement value during the transaction. A depeg, redemption delay, or issuer disruption can affect payment reliability.

Counterparty and custody risk

A stablecoin sandwich may involve payment providers, liquidity providers, exchanges, OTC desks, custodians, banks, and local payout partners.

Businesses need to know who holds funds at each stage, when ownership transfers, and how assets are protected during settlement.

Smart contract and blockchain risk

Simple stablecoin transfers may involve limited technical risk, but more complex flows can rely on smart contracts, bridges, DEXs, or onchain swaps.

Each additional technical layer can introduce bugs, exploits, congestion, or operational failure points.

Data, reporting, and auditability

Institutional users need clear records for every stage: fiat payment, conversion rate, stablecoin amount, wallet address, transaction hash, fees, off-ramp rate, final payout, timestamps, and compliance checks.

Without this reporting layer, stablecoin-based payments can become difficult for finance, compliance, and audit teams to approve at scale.

Who uses stablecoin sandwiches?

Stablecoin sandwiches are mainly used by businesses that need to move value across borders while keeping fiat currency on one or both sides of the transaction.

The model is relevant when the sender does not want to manage a traditional international bank transfer, the recipient does not want to receive crypto, or the payment provider wants to use stablecoin rails in the background to improve settlement.

Payment companies and remittance providers

Payment companies can use stablecoin sandwiches to support faster cross-border settlement and local payouts.

Instead of relying only on correspondent banking chains, they can convert fiat into stablecoins, transfer value onchain, and work with local partners to deliver funds in the recipient’s currency. This can be especially useful in corridors where traditional payment infrastructure is slow, expensive, or difficult to scale.

Marketplaces and global platforms

Marketplaces and digital platforms often need to pay sellers, creators, freelancers, drivers, or contractors across multiple countries.

A stablecoin sandwich can help them move funds between regions while keeping the user experience fiat-based. The platform can fund payments in one currency, use stablecoins for settlement, and let recipients receive local currency through familiar payout methods.

Importers, exporters, and B2B companies

Businesses involved in international trade can use stablecoin sandwiches for supplier payments, treasury transfers, and cross-border settlement.

For these companies, payment predictability matters. Delayed transfers, unclear fees, and limited visibility can create operational friction. Stablecoin-based settlement can help improve timing and transparency, provided there is reliable liquidity and local payout coverage.

Crypto-native companies

Crypto exchanges, brokers, OTC desks, wallets, and Web3 companies often already operate with stablecoins as part of their treasury or settlement stack.

For them, a stablecoin sandwich can connect digital asset balances with fiat obligations. For example, a crypto company may hold USDC or USDT but need to pay vendors, partners, or employees in local currency.

Stablecoin issuers and fintech platforms

Stablecoin issuers and fintech platforms may use sandwich-like flows to support issuance, redemption, distribution, and local market access.

The model can help connect stablecoin liquidity with fiat payment systems, especially when users need to move between digital dollars and local currencies without directly managing the full infrastructure themselves.

Financial institutions and OTC desks

Institutional desks can use stablecoin sandwiches for client settlement, treasury movement, and liquidity management.

For larger flows, the key requirement is not only payment speed. Institutions need reliable quotes, deep liquidity, predictable execution, settlement controls, and clear reporting. This is where the stablecoin sandwich becomes part of broader market infrastructure rather than just a payment method.

Stablecoin sandwich and institutional liquidity

A stablecoin sandwich is often described as a payment model, but for institutional users it is also a liquidity workflow.

The payment may look simple from the outside: fiat goes in, stablecoins move across blockchain rails, and fiat comes out. But behind that flow, someone needs to source liquidity, quote prices, manage conversion risk, and settle both sides of the transaction efficiently.

This is where the quality of liquidity infrastructure becomes critical. The stablecoin transfer itself may be fast, but the real cost and reliability of the payment depend on how well the fiat-to-stablecoin and stablecoin-to-fiat conversions are executed.

Why liquidity determines the real payment cost

The cost of a stablecoin sandwich is not limited to blockchain fees. Businesses also need to consider the spread between fiat and stablecoin, the FX rate used for the final payout, provider fees, slippage, and liquidity availability in the target currency.

For a small payment, these costs may be relatively easy to absorb. For larger B2B or institutional flows, small differences in execution quality can materially affect the final amount received. This is why a stablecoin sandwich should be evaluated as an execution problem, not only a settlement shortcut.

The role of liquidity providers

Liquidity providers help make stablecoin sandwiches work by supplying prices and depth across fiat, stablecoin, and crypto markets.

In a simple flow, this may involve converting USD into USDC and then USDC into BRL, EUR, GBP, or another local currency. In more complex flows, several providers may be needed to support different currencies, regions, settlement methods, and transaction sizes.

The stronger the liquidity network, the easier it is for payment companies and institutional users to offer predictable pricing and reliable payouts.

Why OTC liquidity matters for larger flows

Large transactions are more sensitive to market depth and execution quality.

If a provider does not have enough liquidity for a given currency pair, the transaction may face wider spreads, partial fills, delayed execution, or higher slippage. This can reduce the economic advantage of using stablecoin rails in the first place.

OTC liquidity can help businesses execute larger flows with more predictable pricing and less visible market impact. For payment companies, brokers, and institutional desks, this can be especially important when stablecoin payments are used for treasury movement, client settlement, or high-value cross-border transfers.

Firm pricing vs indicative pricing

Institutional users need to know whether a price is executable. An indicative quote may show a possible rate, but it does not guarantee that the transaction can be completed at that price. In fast-moving or thin markets, this can create uncertainty around the final payout amount.

Firm pricing is more useful for stablecoin sandwich flows because it gives businesses greater confidence in the conversion rate before execution. This is particularly important when a payment provider needs to show the sender or recipient a clear amount in advance.

How fragmented liquidity affects stablecoin payments

Stablecoin liquidity is not evenly distributed across all currencies, regions, and venues. Some pairs are deep and competitive. Others depend on a small number of local providers, banking partners, or OTC desks. This fragmentation can affect pricing, settlement speed, and the ability to scale payment volumes across corridors.

For businesses, the implication is clear: the stablecoin sandwich is only as strong as the liquidity network behind it. To make the model work at scale, companies need access to reliable counterparties, executable quotes, and infrastructure that can connect multiple sources of liquidity efficiently.

How to evaluate a stablecoin sandwich provider

Choosing a stablecoin sandwich provider is not only about finding someone who can move stablecoins onchain. The provider also needs to manage fiat access, liquidity, compliance, settlement, reporting, and local payouts.

For businesses, the most important question is whether the provider can deliver the full payment flow reliably across the corridors they need. A fast blockchain transfer is useful, but it does not help much if the on-ramp is expensive, the off-ramp is weak, or the final payout is hard to reconcile.

Corridor coverage

The first question is which countries, currencies, and payout methods the provider supports.

A provider may offer strong USD and EUR coverage but limited access to local currencies in Latin America, Africa, or Asia. Another may support specific corridors well but lack scale across multiple regions.

Businesses should evaluate both sides of the flow: where funds can be collected, where stablecoins can be settled, and where fiat can be paid out.

Stablecoin and blockchain support

Different providers support different stablecoins and blockchain networks.

Common options may include USDC, USDT, EURC, PYUSD, or other fiat-backed stablecoins. Network support can also vary across Ethereum, Solana, Polygon, Tron, Avalanche, Base, and other chains.

The right choice depends on liquidity, fees, settlement speed, counterparty acceptance, regulatory treatment, and internal treasury policies.

Liquidity depth and execution quality

Liquidity depth determines whether the provider can process transactions at predictable rates.

Businesses should look beyond headline fees and ask how quotes are formed, whether pricing is firm or indicative, what spreads apply, and how larger transactions are handled.

For institutional flows, execution quality can matter more than network fees. A cheap blockchain transfer may still become expensive if the fiat/stablecoin conversion is poorly priced.

Compliance and licensing

A stablecoin sandwich touches both fiat and digital asset infrastructure, so compliance coverage is essential.

Providers should have clear KYC, AML, sanctions screening, transaction monitoring, and recordkeeping processes. Businesses also need to understand which regulated entities are involved in the flow and where they are licensed or registered.

This is especially important for companies operating across multiple jurisdictions or serving their own end customers.

Custody and wallet infrastructure

Businesses should understand who controls the stablecoins during the transaction.

Some providers manage wallets and settlement on behalf of the client. Others allow clients to use their own wallets or custodians. Each model has different implications for security, control, responsibility, and operational complexity.

Key questions include how wallets are secured, who can authorize transfers, whether MPC or qualified custody is available, and how failed or delayed transactions are handled.

Reporting and reconciliation

Stablecoin sandwich flows need clear reporting across both fiat and blockchain legs.

A provider should be able to supply transaction IDs, wallet addresses, timestamps, conversion rates, fees, payout confirmations, customer references, and compliance records.

This is especially important for finance teams. Without clean reporting, the payment may settle quickly but create manual work for accounting, audit, and internal controls.

Integration and API capabilities

For companies processing stablecoin payments at scale, APIs are often as important as pricing.

A strong provider should support automated payment creation, quote requests, transaction monitoring, payout status updates, webhooks, reporting exports, and error handling.

This allows businesses to embed stablecoin sandwich flows into existing payment, treasury, or client-facing systems without relying on manual operations for every transaction.

How Finery Markets supports stablecoin infrastructure

A stablecoin sandwich may look like a payment flow, but at institutional scale it depends on trading infrastructure. Businesses need access to fiat/stablecoin liquidity, reliable cross-rates, executable pricing, settlement workflows, and reporting tools that can support both the onchain and offchain parts of the transaction.

Finery Markets supports this liquidity and execution layer through non-custodial institutional trading infrastructure. The ECN is designed for licensed institutional entities like payment companies, OTC desks and brokers that operate their own environments, maintain their own counterparty relationships, and manage their own compliance, custody, and settlement arrangements.

Institutional liquidity access for stablecoin flows

Finery Markets helps payment companies, brokers and OTC desks connect to a network of liquidity providers and market makers. .

For stablecoin sandwich models, this matters because the payment cost is shaped by the conversion points. Moving from fiat to stablecoin, or from stablecoin back into fiat, requires reliable liquidity across the relevant currency pairs. Finery Markets’ stablecoin infrastructure focuses on improving access to institutional liquidity networks, including support for cross-rate instruments and secondary market trading for stablecoins.

Secondary liquidity for stablecoin issuers and payment use cases

Stablecoin utility depends on more than issuance. A token also needs a functioning secondary market where institutions can trade it efficiently against fiat currencies, other stablecoins, and crypto assets.

Finery Markets helps stablecoin issuers create secondary market trading for their assets, connecting with institutional market makers. This can be especially relevant for stablecoin-powered payment models where liquidity depth, pricing consistency, and market access determine whether the flow can scale.

Multiple trading mechanisms for better execution

Different stablecoin sandwich use cases may require different execution models. Some flows need firm order-book liquidity. Others may require RFQ, quote streams, or API-driven access to multiple liquidity providers.

Finery Markets supports multiple trading mechanisms, including an aggregated order book, RFQ, and quote streams. This gives institutional clients more flexibility in how they source liquidity, route orders, and manage execution across stablecoin and fiat-linked markets.

White-label infrastructure for client-facing stablecoin products

For businesses that want to offer crypto and stablecoin trading under their own brand, Finery Markets provides FM White Label — a fully branded B2B crypto trading platform that can be launched in under a week.

This can be relevant for brokers, payment providers, OTC desks, and fintech platforms that want to build client-facing stablecoin or crypto trading services without developing the full trading stack internally. FM White Label includes branded GUI and API endpoints, spread and markup management, multi-role account access, reporting, and support for spot and non-deliverable products.

Settlement, reporting, and operational controls

Stablecoin sandwich workflows require more than execution. Institutions also need settlement records, wallet and bank account controls, reporting, and auditability.

Finery Markets’ infrastructure includes flexible settlement tools, verified address-book functionality for wallets and bank accounts, role-based access, risk controls, and reporting through GUI or API. These features can help institutional clients manage the operational side of stablecoin-related trading and settlement workflows.

A non-custodial infrastructure layer

Finery Markets does not replace the regulated payment provider, custodian, bank, or local payout partner in a stablecoin sandwich. Those functions remain with the institutional client and its chosen counterparties.

Its role is to provide the technology layer for institutional liquidity access, execution, white-label trading, settlement workflows, and reporting. For stablecoin sandwich models, this layer can help make fiat/stablecoin conversion more efficient, transparent, and scalable.

The future of stablecoin sandwiches

The stablecoin sandwich is likely to become more common as businesses look for faster and more flexible ways to move value across borders. But its future will not depend on stablecoins alone. It will depend on the development of regulated issuers, deeper liquidity, better fiat on- and off-ramps, and institutional-grade infrastructure around execution, custody, compliance, and reporting.

Over time, the stablecoin layer may also become less visible to end users. A company may send dollars, a supplier may receive reals, and neither side may need to know that stablecoins were used for settlement in the middle. In that scenario, stablecoins become backend infrastructure rather than a front-end payment experience.

More regulated payment stablecoins

As stablecoin regulation becomes more defined, institutional adoption may accelerate.

Clearer rules can help banks, payment companies, brokers, fintech platforms, and corporate treasury teams understand which stablecoins they can use, what reserves stand behind them, how redemptions work, and what obligations apply to service providers.

At the same time, regulation may raise the bar for market participants. Stablecoin payment models will need stronger compliance controls, better reporting, clearer customer disclosures, and more disciplined risk management.

Growth of local currency stablecoins

Most stablecoin liquidity today is concentrated around U.S. dollar-denominated assets. That makes sense given the dollar’s role in global trade and crypto markets, but it also limits how efficiently stablecoin sandwiches can work in some local corridors.

As more local currency stablecoins emerge, businesses may be able to reduce reliance on repeated USD-based conversions. For example, a payment flow could eventually use more direct stablecoin liquidity between local currencies, rather than always routing through a dollar stablecoin.

This could make some corridors faster and more cost-efficient, but only if local stablecoins develop enough liquidity, regulatory clarity, issuer trust, and institutional adoption.

Integration with payment platforms and banks

Stablecoin sandwiches may increasingly be embedded into payment platforms, fintech products, banking services, and treasury tools.

This matters because most businesses do not want to manage blockchain infrastructure directly. They want reliable payments, clear reporting, predictable pricing, and compliant settlement. If providers can abstract the stablecoin layer, adoption becomes easier.

In this model, stablecoins become part of the payment stack in the same way other settlement technologies are used today: important to the infrastructure provider, but largely invisible to the end user.

Stablecoins as backend settlement infrastructure

The long-term potential of the stablecoin sandwich is not that every business will start holding stablecoins on its balance sheet.

A more realistic outcome is that stablecoins become one of several backend settlement options used by payment companies, OTC desks, fintech platforms, brokers, and financial institutions. They may be used when they offer better speed, cost, liquidity access, or operating hours than traditional rails.

For institutional users, the winning model will not be simply “crypto instead of banks.” It will be a hybrid structure where fiat systems, stablecoin rails, liquidity providers, and regulated financial infrastructure work together.

FAQ

What is a stablecoin sandwich?

A stablecoin sandwich is a payment flow where fiat currency is converted into a stablecoin, transferred onchain, and then converted back into fiat currency for the recipient.

The structure is simple: Fiat → stablecoin → fiat

This allows businesses to use stablecoin rails for settlement while keeping the sender and recipient connected to local currency systems.

Why is it called a stablecoin sandwich?

It is called a stablecoin sandwich because the stablecoin sits in the middle of the transaction.

Fiat currency is used at the beginning and end of the payment, while the stablecoin acts as the settlement layer between the two fiat systems.

How does a stablecoin sandwich work?

A stablecoin sandwich usually has three stages.

First, the sender’s fiat currency is converted into a stablecoin. Second, the stablecoin is transferred over a blockchain network. Third, the stablecoin is converted into the recipient’s local fiat currency and paid out through local rails.

Is a stablecoin sandwich faster than a bank transfer?

It can be faster, especially for the settlement leg of the transaction.

Stablecoins can move 24/7 across blockchain networks, while traditional bank transfers may depend on banking hours, correspondent banks, cut-off times, and local holidays. However, the full payment speed also depends on fiat on-ramps, off-ramps, compliance checks, and local payout infrastructure.

Is a stablecoin sandwich cheaper than traditional cross-border payments?

It can be cheaper in some corridors, but not always.

A stablecoin sandwich may reduce intermediary banking fees and improve settlement efficiency. At the same time, businesses still need to account for conversion spreads, provider fees, blockchain network fees, payout costs, and liquidity conditions.

The final cost depends on execution quality across the full flow.

What is the difference between a stablecoin sandwich and a stablecoin sundae?

A stablecoin sandwich usually follows a simple structure:

Fiat → stablecoin → fiat

A stablecoin sundae is more layered. It may involve local-currency stablecoins and onchain swaps, for example:

Fiat → local stablecoin → foreign stablecoin → fiat

The sundae model can offer more flexibility in theory, but it also adds more conversion points, liquidity requirements, and technical complexity.

What is an open stablecoin sandwich?

An open stablecoin sandwich is a flow where one side remains in stablecoins.

For example, the sender may pay in fiat while the recipient receives stablecoins, or the sender may pay in stablecoins while the recipient receives fiat.

This model can work when one party is already comfortable holding or using stablecoins directly.

What stablecoins are used in stablecoin sandwiches?

Common stablecoins used in these flows include dollar-backed stablecoins such as USDC and USDT, as well as euro-backed or other fiat-backed stablecoins where liquidity and regulatory conditions allow.

The choice depends on liquidity, issuer reliability, redemption options, blockchain support, counterparty acceptance, and local regulatory treatment.

What are the main risks of stablecoin sandwich payments?

The main risks include regulatory uncertainty, AML and sanctions compliance, stablecoin issuer risk, liquidity gaps, custody risk, blockchain risk, FX spread, and reporting complexity.

For businesses, the key challenge is not just moving stablecoins onchain. It is managing the full payment process across fiat conversion, execution, settlement, compliance, and reconciliation.

Who can use a stablecoin sandwich?

Stablecoin sandwiches can be used by payment companies, remittance providers, marketplaces, fintech platforms, importers, exporters, crypto-native companies, OTC desks, brokers, and financial institutions.

The model is most relevant for businesses that need cross-border settlement while keeping fiat currency at one or both ends of the transaction.

How do liquidity providers support stablecoin sandwich transactions?

Liquidity providers support the conversion points in the flow.

They help businesses move from fiat into stablecoins and from stablecoins back into fiat or other assets. Their role is especially important for larger transactions, less liquid currencies, and corridors where pricing, depth, and execution quality determine whether the payment model is commercially viable.

.png)