Stablecoin FX refers to the exchange of fiat-pegged digital assets across currencies, usually on blockchain-based rails. In simple terms, it is foreign exchange where at least one side of the transaction involves a stablecoin — for example, converting USDC into EURC, moving from a local currency into a USD stablecoin, or using stablecoins as an intermediate settlement layer in a cross-border payment.

The concept is becoming more relevant because stablecoins are no longer just a bridge asset for crypto trading. According to Finery Markets’ Crypto OTC Trading Report 2026, stablecoins’ share of institutional OTC transaction volume rose from 23% in 2023 to 78% in 2025. Over the same period, institutional spot OTC volumes expanded by 109% year-over-year, compared with just 9% growth across top-20 centralized exchanges. The data points to a broader market shift: institutions are moving more activity into OTC environments, while stablecoins are becoming the default settlement layer for that activity.

This shift is also visible at the market level. Stablecoin market capitalization reached approximately $310 billion in January 2026, while annual transaction volume exceeded $57 trillion. For businesses that need to move value across regions, currencies, and counterparties, stablecoins offer a different operating model: faster settlement, extended market availability, greater transparency, and more flexible access to liquidity than many traditional payment rails.

Stablecoin FX does not replace traditional FX. The conventional FX market remains far larger, deeper, and more mature. But stablecoin FX introduces a new execution and settlement layer for specific use cases where traditional banking infrastructure can be slow, expensive, or operationally fragmented.

In this article, we explain what stablecoin FX is, how it works, where it creates practical value, and what risks institutions need to manage before adding stablecoins to their FX, payments, or treasury stack.

What is stablecoin FX?

Stablecoin FX is the exchange of fiat-pegged digital assets across different currencies. Instead of exchanging only traditional fiat currencies, such as USD, EUR, GBP or BRL, stablecoin FX involves tokenized representations of those currencies, typically issued on blockchain networks.

At its simplest, stablecoin FX can mean exchanging one stablecoin for another. For example, a business may convert a USD-backed stablecoin into a euro-backed stablecoin, such as USDC to EURC. In another case, a payment provider may receive local fiat currency from a client, convert it into a USD stablecoin, move the value onchain, and then convert it back into local fiat at the destination.

This is why stablecoin FX sits between three markets: foreign exchange, digital assets, and cross-border payments. It uses the logic of FX, because value is converted between currency denominations. It uses stablecoins, because the assets are blockchain-based tokens designed to track fiat currencies. And it often serves payment or treasury use cases, because the goal is not always speculative trading, but faster settlement, liquidity movement, or operational efficiency.

The most important distinction is that stablecoin FX changes the settlement layer. In traditional FX, execution and settlement usually rely on banks, correspondent networks, clearing systems, cut-off times, and multi-day post-trade processes. In stablecoin FX, at least part of the value movement can happen on blockchain rails, allowing participants to transfer fiat-denominated value with greater speed, transparency, and availability.

This does not remove the need for fiat banking infrastructure. Most real-world flows still require on-ramps, off-ramps, local payout partners, compliance controls, and liquidity providers. But it can reduce the number of steps involved in moving value between counterparties and jurisdictions.

In practice, stablecoin FX can take several forms:

-

fiat to stablecoin, such as BRL to USDC

-

stablecoin to fiat, such as USDC to EUR

-

stablecoin to stablecoin, such as USDC to EURC

-

fiat to stablecoin to fiat, often described as a stablecoin sandwich

The broader idea is simple: stablecoins are becoming a programmable settlement layer for currency movement. Stablecoin FX is the market structure that allows those currency-linked digital assets to be priced, exchanged, settled, and used in institutional workflows.

How stablecoin FX works

Stablecoin FX usually starts with a simple business need: one party has value in one currency and needs to deliver value in another. The difference is that the conversion and settlement process can use stablecoins as part of the transaction flow.

A typical stablecoin FX transaction includes three layers: fiat access, digital asset liquidity, and settlement.

.png)

The first layer is the on-ramp. This is where fiat currency enters the stablecoin environment. A payment provider, broker, OTC desk, or treasury team may convert local currency into a stablecoin through a regulated partner, liquidity provider, exchange, or institutional trading venue. For example, a company may convert BRL, MXN, EUR, or GBP into a USD-backed stablecoin.

The second layer is execution. Once the transaction enters the digital asset environment, the participant needs pricing and liquidity. This can happen through different execution models, including RFQ, quote streams, order books, OTC liquidity, or automated market makers. For institutional use cases, the quality of execution matters as much as speed. Participants need reliable pricing, sufficient market depth, and predictable settlement outcomes, especially when handling larger client or treasury flows.

The third layer is settlement. After execution, the stablecoin can be transferred onchain to another wallet, trading venue, settlement network, or payout partner. Depending on the use case, the recipient may hold the stablecoin, convert it into another stablecoin, or off-ramp it into local fiat currency.

A simple cross-border payment flow may look like this:

Local fiat → USD stablecoin → local fiat

A more direct stablecoin FX flow may look like this:

USD stablecoin → EUR stablecoin

In the first case, the stablecoin acts as a bridge between two fiat currencies. In the second case, the FX transaction happens directly between two fiat-pegged digital assets.

This is why stablecoin FX is not only about the asset itself. It is about the infrastructure around the asset: liquidity providers, fiat rails, custody or wallet controls, compliance checks, settlement logic, reporting, and reconciliation. Without this infrastructure, stablecoins may move quickly onchain, but the overall transaction can still fail operationally.

For institutions, the main question is not whether stablecoins can be transferred from one wallet to another. They can. The harder question is whether stablecoin-based FX flows can be executed with reliable pricing, controlled counterparty risk, compliant settlement, and clear post-trade records.

Stablecoin FX and the stablecoin sandwich

One of the most common stablecoin FX flows is the stablecoin sandwich: a cross-border payment structure where fiat currency is converted into a stablecoin, transferred onchain, and then converted back into fiat currency for the recipient.

The basic structure is:

local fiat currency → stablecoin → local fiat currency

For example, a U.S.-based company may need to pay a supplier, contractor, or local partner in Brazil. In a traditional payment flow, the company may send USD through one or more correspondent banks before the funds are converted into Brazilian reals and delivered to the recipient. In a stablecoin sandwich flow, the company or its payment provider can convert USD into USDC, transfer USDC over blockchain rails, and then convert USDC into BRL through a local liquidity or payout partner.

In this model, the stablecoin is not necessarily visible to the sender or recipient. The sender may only see a fiat debit, and the recipient may only see a fiat credit. The stablecoin sits in the middle as the settlement layer, while the business workflow remains connected to local currency systems on both sides.

This is why the stablecoin sandwich is especially relevant for payment companies, fintech platforms, marketplaces, OTC desks, and institutional businesses that want to benefit from blockchain-based settlement without requiring end users to hold stablecoins directly. Businesses still invoice, pay taxes, manage payroll, and reconcile accounts in fiat. Stablecoins simply change how value moves between the two fiat endpoints.

Stablecoin FX appears at the conversion points. The first conversion happens when fiat is exchanged for a stablecoin at the origin. The second happens when the stablecoin is exchanged for fiat at the destination. The final economics depend on execution quality across both legs: quoted rates, spreads, provider fees, blockchain network costs, local liquidity, transaction size, and payout infrastructure.

This is also where many operational risks remain. The onchain transfer may settle in seconds or minutes, but the full payment experience still depends on fiat on-ramps, off-ramps, compliance screening, sanctions checks, transaction monitoring, liquidity sourcing, custody or wallet infrastructure, and reconciliation records. A fast blockchain transaction does not automatically mean instant fiat delivery.

The stablecoin sandwich is only one model within stablecoin FX. An open sandwich keeps one side of the transaction in stablecoins, such as fiat → stablecoin or stablecoin → fiat. A one-legged stablecoin transaction involves only one fiat conversion. A more layered model, sometimes described as a stablecoin sundae, may involve local stablecoins, onchain swaps, foreign stablecoins, and fiat payout.

For most institutions, the choice of model depends on corridor coverage, regulatory requirements, liquidity depth, accounting needs, and the quality of the on-ramp and off-ramp. The structure only works if the business can convert in and out of stablecoins reliably, at predictable rates, and with the required compliance controls.

Stablecoin FX vs traditional FX

Stablecoin FX borrows the basic logic of foreign exchange, but changes the infrastructure around execution and settlement.

In traditional FX, currencies are exchanged through a mature network of banks, brokers, trading venues, market makers, clearing systems, and settlement providers. The market is deep, highly liquid, and essential to global finance. For major currency pairs, traditional FX remains far more developed than any stablecoin-based alternative.

The friction usually appears after the trade. Cross-border payments and treasury transfers can still depend on correspondent banking chains, local cut-off times, bank holidays, manual compliance handoffs, and multi-step reconciliation. Even when pricing is competitive, the operational path between sender and recipient may be slow or difficult to control.

Stablecoin FX introduces a different model. Instead of moving value only through bank-led rails, participants can use fiat-pegged digital assets as part of the transaction flow. This can make settlement faster, extend availability beyond banking hours, and provide a more transparent record of value movement.

The main difference is not that stablecoin FX creates a better exchange rate by default. In many cases, the opposite can be true if liquidity is thin, spreads are wide, or on- and off-ramp costs are high. The value comes from the ability to change how currency-linked value moves, settles, and reconciles across systems.

For payment providers and treasury teams, this distinction matters. A stablecoin-based flow may reduce the need to pre-fund accounts in multiple jurisdictions, improve capital mobility, or support faster payout cycles. But it may also introduce new dependencies: issuer risk, blockchain network risk, custody controls, local regulatory requirements, and the availability of reliable liquidity in each corridor.

The practical comparison is therefore not “traditional FX or stablecoin FX.” It is more specific: which rail is more efficient for a particular corridor, transaction size, settlement requirement, counterparty, and compliance setup?

In highly liquid fiat corridors, traditional FX may remain the better choice. In high-friction corridors, payment-heavy workflows, digital asset settlement, or situations where speed and liquidity mobility matter more than legacy process familiarity, stablecoin FX can create a meaningful operational advantage.

Main use cases for stablecoin FX

Stablecoin FX is most useful in workflows where currency conversion, settlement speed, liquidity mobility, and operational control matter at the same time. This is why adoption is being driven less by speculative trading and more by payments, treasury, OTC execution, and institutional settlement.

Cross-border payments

Cross-border payments are one of the clearest use cases. Payment providers can use stablecoins as a settlement layer between two fiat endpoints, helping clients move value across jurisdictions without relying entirely on correspondent banking chains.

This can be especially relevant in corridors where traditional transfers are slow, expensive, or difficult to reconcile. Stablecoins can shorten settlement time, provide clearer transaction visibility, and reduce the need for multiple intermediaries. The end customer may still send and receive fiat, while the provider uses stablecoins to move value behind the scenes.

Treasury operations

Treasury teams can use stablecoin FX to move liquidity between entities, regions, or platforms faster than traditional bank transfers may allow. This can support cash concentration, internal funding, working capital management, and short-term liquidity rebalancing.

For companies operating across multiple markets, the ability to move fiat-denominated value outside banking cut-off windows can be useful. Stablecoin FX can also help treasury teams reduce idle balances in pre-funded accounts, although this depends on the quality of on- and off-ramp coverage in each market.

OTC trading and institutional settlement

OTC desks, brokers, and liquidity providers can use stablecoin FX to support clients that want to settle trades in different stablecoins or move between fiat and digital asset liquidity. In institutional crypto markets, stablecoins already play a central role as settlement assets, especially for spot trading and OTC flows.

Stablecoin FX allows these businesses to offer more flexible settlement options. A client may want to buy crypto with fiat, settle proceeds in a USD stablecoin, convert into a euro stablecoin, or off-ramp into local currency. Each of these workflows requires reliable pricing, execution, and post-trade settlement.

Broker and payment provider liquidity management

Brokers and payment providers often need to maintain balances across multiple currencies, jurisdictions, and counterparties. Stablecoin FX can help them rebalance liquidity more efficiently, especially when client demand changes quickly or when local banking rails are unavailable outside business hours.

Instead of holding large pre-funded balances in every market, a business may use stablecoins to move liquidity where it is needed. This can improve capital efficiency, but only when the business has access to institutional-grade liquidity, compliant settlement channels, and reliable fiat payout partners.

Stablecoin issuer and ecosystem liquidity

For stablecoin issuers, liquidity is not only about primary minting and redemption. A stablecoin also needs healthy secondary markets if institutions are expected to use it at scale.

Stablecoin FX can support this by creating more reliable conversion paths between different currency-linked stablecoins and between stablecoins and fiat currencies. Without this liquidity, a stablecoin may be technically available but difficult to use in real institutional workflows.

Emerging-market dollar access

Stablecoin FX also plays an important role in markets where access to dollar liquidity is limited, expensive, or fragmented. Businesses and users may use USD-backed stablecoins as an alternative way to hold or transfer dollar-denominated value.

This can create practical benefits for payments and treasury, but it also raises important policy and market-structure questions. When stablecoin flows become large enough, they may interact with local FX markets, local currency demand, and funding conditions. For institutions, this makes risk controls and corridor-level analysis essential.

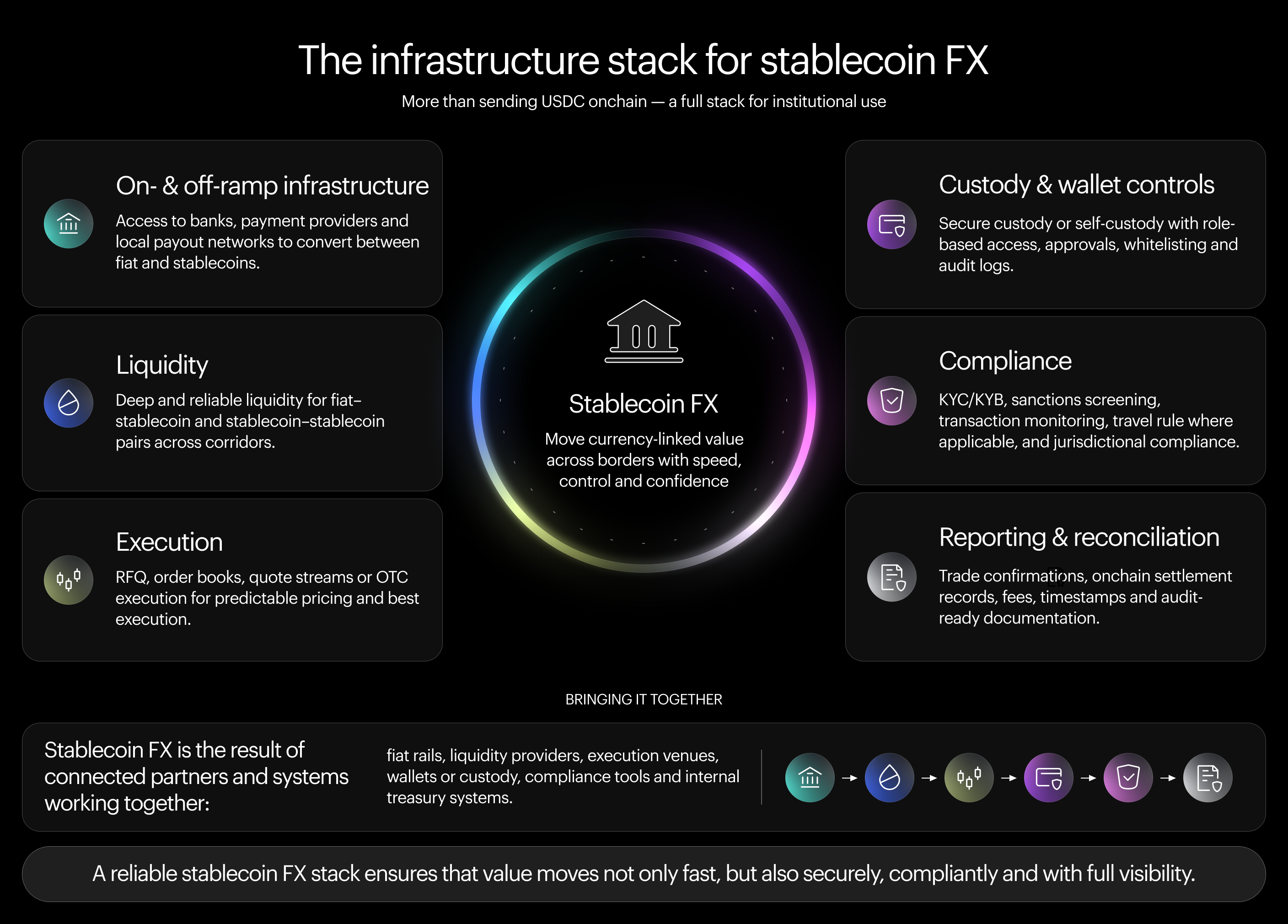

What infrastructure is needed for stablecoin FX?

Stablecoin FX depends on more than access to a blockchain wallet. For institutional use, it requires a full stack that can support pricing, execution, settlement, compliance, custody, reporting, and fiat connectivity.

The first requirement is reliable on- and off-ramp infrastructure. Most stablecoin FX flows still begin or end in fiat currency, which means businesses need access to banking partners, payment providers, local payout networks, and regulated conversion channels. Without dependable fiat connectivity, the onchain part of the transaction may be fast, but the overall payment or treasury flow can still be delayed.

The second requirement is liquidity. Stablecoin FX needs market makers, OTC desks, trading venues, or liquidity providers that can quote stablecoin pairs and fiat-stablecoin pairs with sufficient depth. This is especially important for larger transactions, less liquid corridors, or non-USD stablecoins, where spreads can widen quickly if market depth is limited.

Execution infrastructure is another key layer. Institutional participants may use RFQ, order books, quote streams, or OTC execution depending on transaction size, urgency, and liquidity conditions. For payment providers and brokers, predictable execution is critical because client pricing often depends on tight spreads and reliable settlement outcomes.

Custody and wallet controls also matter. Businesses need secure wallet infrastructure, role-based access, transaction approval policies, withdrawal rules, whitelisting, and audit logs. Whether assets are held in custody, self-custody, or moved through non-custodial workflows, the operational controls must match institutional risk standards.

Compliance is equally important. Stablecoin FX may involve digital assets, payments, FX activity, cross-border transfers, and local payout obligations. This means firms need KYC and KYB checks, sanctions screening, transaction monitoring, travel rule processes where applicable, and clear jurisdictional analysis for each corridor.

The final layer is reporting and reconciliation. Institutional users need trade confirmations, settlement records, transaction IDs, fees, timestamps, counterparty information, accounting treatment, and audit-ready documentation. For a payment provider processing high volumes, reconciliation can be just as important as settlement speed.

In practice, a stablecoin FX stack usually combines several partners and systems: fiat rails, liquidity providers, execution venues, wallet or custody infrastructure, compliance tools, and internal treasury or accounting systems. The more complex the flow, the more important it becomes to orchestrate these components through a controlled, auditable workflow.

This is where the institutional version of stablecoin FX differs from a retail crypto transfer. The goal is not only to move tokens from one address to another. The goal is to move currency-linked value between counterparties in a way that is liquid, compliant, secure, predictable, and easy to reconcile.

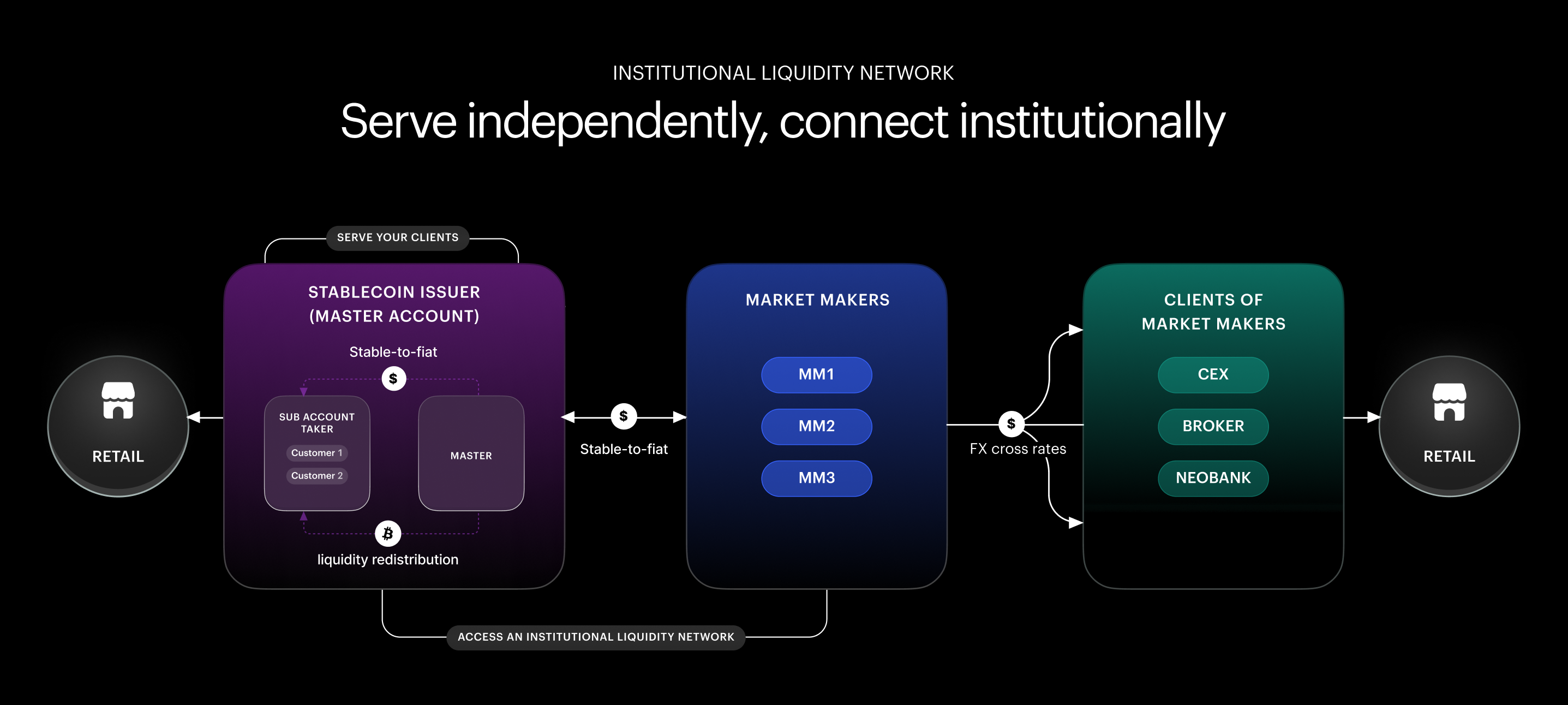

Finery Markets: One-step stablecoin FX infrastructure

For stablecoin FX to work at institutional scale, businesses need more than issuance, custody, or wallet connectivity. They need access to secondary liquidity: the market structure that allows stablecoins to be priced, exchanged, and used across real trading, payment, and treasury workflows.

This is where Finery Markets provides a core infrastructure layer for stablecoin issuers, payment providers, OTC desks, brokers, banks, and liquidity providers. Through non-custodial SaaS technology, Finery Markets helps institutional participants connect to liquidity, create stablecoin cross-rate instruments, and support secondary market trading for fiat-stablecoin, stablecoin-stablecoin, and crypto-stablecoin pairs.

For stablecoin issuers, secondary liquidity is often the missing link between launching a token and making it useful. A stablecoin may have a strong primary market setup, including regulation, reserve management, banking relationships, and mint/burn policies. But without active secondary markets, institutional users may still struggle to convert the asset efficiently, especially in larger transaction sizes or less liquid corridors.

Finery Markets addresses this problem by connecting stablecoin issuers to an institutional liquidity network. This includes access to market makers, liquidity providers, payment companies, OTC desks, brokers, banks, and other professional counterparties that can help create deeper, more reliable markets around a stablecoin.

The infrastructure is designed to support several components that are critical for stablecoin FX:

-

cross-rates between stablecoins, fiat currencies, and crypto assets

-

access to institutional market makers and liquidity providers

-

RFQ, order book, and quote-stream trading mechanisms

-

API-first integration for automated trading and payment workflows

-

multi-currency settlement corridor coverage

-

non-custodial workflows where counterparties maintain their own bilateral relationships

-

reporting, position management, and risk-management capabilities

This matters because stablecoin FX depends on predictable execution. Payment providers need to know whether they can convert stablecoins into local payout currencies at scale. OTC desks need reliable pricing across client settlement assets. Stablecoin issuers need their assets to move beyond passive circulation and into active institutional use cases.

A practical example is euro-denominated stablecoin liquidity. In a market still dominated by USD stablecoins, European institutions may face unwanted FX exposure when using dollar-linked assets for euro-based operations. By connecting euro stablecoin issuers to institutional market makers and payment flows, secondary liquidity infrastructure can help create more efficient onchain FX routes for EUR-based settlement.

In this sense, Finery Markets does not only support trading activity around stablecoins. It helps stablecoins become more usable as financial infrastructure. The goal is to turn a stablecoin from a minted asset into a liquid, accessible, and institution-ready instrument that can support payments, OTC trading, treasury operations, and cross-border settlement.

Benefits of stablecoin FX

The main benefit of stablecoin FX is not only faster blockchain settlement. Its value comes from combining currency conversion, digital asset liquidity, and programmable settlement into one operational workflow.

For institutions, this can create advantages across several areas: speed, availability, transparency, capital efficiency, and operational control.

Faster settlement

Stablecoin transfers can settle much faster than many traditional cross-border payment flows. Instead of waiting for correspondent banking chains, cut-off windows, or multi-day settlement cycles, businesses can move stablecoins across blockchain networks in minutes or, in some cases, seconds.

This can be useful for payment providers, OTC desks, brokers, and treasury teams that need to move value quickly between counterparties, venues, or regions. Faster settlement also reduces the time during which capital is stuck in transit.

24/7 availability

Traditional banking and FX infrastructure still depends on business hours, weekends, holidays, and local settlement windows. Stablecoin rails can operate continuously, which gives institutions more flexibility when managing global liquidity.

This matters in digital asset markets, where trading activity continues outside traditional market hours. It also matters for global businesses operating across time zones, where waiting for the next banking day can slow down payouts, liquidity rebalancing, or client settlement.

Greater transparency

Stablecoin transactions can provide a clear onchain record of value movement. This can make it easier to track whether funds have been sent, received, or settled, especially compared with payment flows that pass through multiple intermediaries.

Transparency does not remove the need for internal reporting or compliance documentation. But it can improve visibility into settlement status and help reduce uncertainty during the transaction lifecycle.

Better capital efficiency

Stablecoin FX can help businesses reduce reliance on pre-funded balances across multiple jurisdictions. Instead of holding idle liquidity in many local accounts, a company may use stablecoins to move value where it is needed, when it is needed.

This can support more efficient treasury operations, especially for businesses managing global payouts, OTC settlement, or multi-entity cash flows. The benefit depends on reliable liquidity, corridor coverage, and the ability to convert in and out of fiat when required.

More flexible liquidity movement

Stablecoins can move between wallets, trading venues, liquidity providers, and settlement partners more easily than traditional bank balances. This gives institutions more flexibility when routing liquidity across different platforms and counterparties.

For brokers and OTC desks, this can support faster client settlement. For payment providers, it can improve the ability to respond to demand in specific corridors. For treasury teams, it can make liquidity rebalancing more dynamic.

Operational efficiency

Stablecoin FX can reduce some of the manual work associated with cross-border settlement, including payment tracking, reconciliation, and confirmation of receipt. When integrated properly, stablecoin-based workflows can connect execution, settlement, and reporting more directly.

This is especially relevant for high-volume businesses where small operational improvements can compound across thousands of transactions.

The benefits, however, are not automatic. Stablecoin FX only creates institutional value when the full workflow is reliable: pricing, liquidity, fiat access, compliance, custody, settlement, and reconciliation all need to work together. Without that infrastructure, faster onchain movement may simply shift friction from one part of the process to another.

Risks and limitations of stablecoin FX

Stablecoin FX can improve speed, transparency, and liquidity movement, but it also introduces risks that do not exist in the same form in traditional FX. For institutions, the question is not whether stablecoin FX is useful. The question is whether the full workflow can be controlled across liquidity, settlement, custody, compliance, and accounting.

Liquidity risk

Liquidity is the first practical limitation. USD stablecoins are widely traded, but liquidity is much less consistent across non-USD stablecoins, local fiat pairs, and emerging-market corridors.

If liquidity is thin, execution costs can rise quickly. Spreads may widen, larger orders may move the market, and conversions may fail or require manual routing through multiple venues. This is why institutional stablecoin FX depends on access to deep liquidity providers, live market depth, and execution controls such as slippage limits and fallback routing.

Issuer and redemption risk

Stablecoins depend on the quality of the issuer, reserve structure, redemption process, and banking relationships behind the token. If a stablecoin loses confidence, trades away from its peg, or faces redemption delays, the impact can move through payment, trading, and treasury workflows.

This is especially important when stablecoins are used as a bridge asset. Even if the stablecoin is held only briefly, the business still has exposure during the transaction lifecycle. Institutions need to understand issuer terms, reserve disclosures, redemption mechanics, and backup liquidity options before relying on a stablecoin for operational flows.

Peg and pricing risk

Stablecoins are designed to track fiat currencies, but they do not always trade exactly at par. In stressed markets, during liquidity shortages, or in less efficient corridors, the price of acquiring dollar exposure through a stablecoin can differ from the price of acquiring dollars through traditional FX.

These gaps matter for stablecoin FX because they affect the real cost of conversion. A payment provider may expect a stablecoin to behave like a digital dollar, but the final execution price can still depend on market depth, local demand, and the availability of arbitrage between crypto and traditional FX venues.

Counterparty risk

Stablecoin FX workflows often involve several counterparties: issuers, liquidity providers, OTC desks, exchanges, custodians, banks, payment processors, and local payout partners. Each one introduces operational and credit exposure.

For institutions, counterparty selection becomes part of the FX workflow. It is not enough to have access to a quote. Businesses need to know who provides liquidity, who controls settlement, who holds assets, what happens if a partner fails, and how disputes or failed transactions are handled.

Custody and wallet risk

Stablecoin FX requires secure movement of digital assets. This creates risks around private keys, wallet access, transaction approvals, withdrawal rules, address whitelisting, and internal fraud.

Institutional setups need strong policy controls, role-based permissions, audit logs, and clear responsibility for transaction approval. In payment or treasury workflows, even a small operational mistake can create an irreversible settlement problem.

Regulatory and compliance risk

Stablecoin FX can touch several regulated activities at once: digital assets, payment services, money transmission, FX, custody, sanctions screening, and cross-border value transfer. The regulatory treatment can vary significantly by jurisdiction.

This means institutions need corridor-level analysis. A flow that is viable in one market may require licensing, additional controls, or different counterparties in another. Compliance must be built into the workflow rather than added after execution.

Accounting and reconciliation risk

A stablecoin FX transaction can generate several records: the original fiat movement, the stablecoin trade, the onchain transfer, the off-ramp, fees, timestamps, exchange rates, and final payout. If these records are not connected properly, finance teams may struggle to reconcile the flow.

Accounting treatment can also vary depending on jurisdiction, asset type, holding period, and internal policy. Institutions need valuation logic, peg variance tracking, audit trails, and documentation that finance and compliance teams can rely on.

Market spillover risk

As stablecoin FX grows, it may also interact more directly with traditional FX markets. Research from the IMF and BIS has documented that stablecoin-based FX flows can create parity deviations between stablecoin and traditional FX venues and may be linked to local currency pressure and dollar funding conditions.

For payment companies and institutional trading businesses, this reinforces a simple point: stablecoin FX is not isolated from the broader financial system. Liquidity, pricing, and risk management need to account for both the onchain market and the traditional FX market around it.

Stablecoin FX is therefore best understood as an infrastructure decision, not only a payment innovation. The benefits are real, but they depend on whether the institution can manage the full operating model with the same discipline it would apply to any other financial market infrastructure.

The future of stablecoin FX

Stablecoin FX is still early, but its direction is becoming clearer. The market is moving from simple fiat-stablecoin conversions toward more developed liquidity networks where stablecoins can be exchanged, routed, and settled across multiple currencies and counterparties.

Today, most activity is still centered around USD-backed stablecoins. This reflects the broader role of the dollar in both traditional finance and digital asset markets. For many institutions, USD stablecoins remain the most liquid and practical settlement asset available.

But the next phase of stablecoin FX is unlikely to be USD-only. Euro-denominated stablecoins are already showing signs of institutional traction. In Finery Markets’ Crypto OTC Review for Q1 2026, EURC emerged as the fastest-growing asset in the segment, recording +41x year-over-year growth. The same report found that stablecoin volumes increased by 59% YoY, while stablecoins accounted for 82% of total OTC trades in Q1 2026.

This matters because EUR stablecoins can reduce the need for European institutions to rely on dollar-linked assets for euro-denominated workflows. A broker, payment provider, or OTC desk operating in Europe may not always want to introduce USD exposure into a transaction that starts and ends in euros. As euro stablecoin liquidity improves, stablecoin FX can support more direct routes for EUR-based settlement, treasury rebalancing, and institutional trading.

Regulation is also pushing the market in this direction. MiCA-driven delistings of non-compliant USD stablecoins have accelerated interest in euro-denominated alternatives, creating a clearer path for regulated EUR stablecoins to become part of institutional market infrastructure.

Over time, this could change the structure of cross-border payments and digital asset settlement. In the first phase, stablecoins often worked as a hidden settlement rail between two fiat endpoints. In the next phase, stablecoin FX may become a more active liquidity layer, where payment companies, brokers, OTC desks, banks, and fintech platforms route between different fiat-pegged assets depending on price, depth, speed, and regulatory suitability.

The market will also need more institutional infrastructure. Stablecoin FX cannot scale only through fragmented exchange books or manual OTC workflows. It will require better liquidity aggregation, firm pricing, API-based execution, automated settlement, risk controls, compliant counterparties, and reliable reporting. In other words, the future of stablecoin FX depends less on the existence of stablecoins themselves and more on the quality of the market infrastructure around them.

Stablecoin FX is unlikely to replace traditional FX. The conventional market is too large, liquid, and deeply embedded in global finance. But stablecoin FX can become a parallel settlement and liquidity layer for specific use cases: cross-border payments, digital asset trading, treasury rebalancing, emerging-market settlement, and multi-currency stablecoin liquidity.

The long-term opportunity is not simply to make payments faster. It is to make currency movement more programmable, more transparent, and more directly connected to the systems where digital finance already operates.

Stablecoin FX FAQ

What does stablecoin FX mean?

Stablecoin FX means exchanging fiat-pegged digital assets across currencies. This can include converting one stablecoin into another, such as USDC to EURC, or using a stablecoin as part of a fiat-to-fiat cross-border payment flow.

Is stablecoin FX the same as traditional FX?

No. Traditional FX involves exchanging fiat currencies through banks, brokers, trading venues, and settlement systems. Stablecoin FX uses fiat-pegged digital assets and blockchain-based settlement as part of the transaction flow. It follows the logic of FX, but uses different infrastructure.

What is an example of stablecoin FX?

A simple example is converting USDC into EURC. Another example is a payment provider converting local fiat into USDC, transferring USDC onchain, and then converting it into local fiat for the recipient.

Why are stablecoins used in FX transactions?

Stablecoins can make currency-linked value easier to move across platforms, counterparties, and jurisdictions. They can support faster settlement, 24/7 availability, improved transparency, and more flexible liquidity management compared with some traditional payment rails.

What is the difference between stablecoin FX and a stablecoin sandwich?

A stablecoin sandwich is one type of stablecoin FX flow. It describes a transaction where fiat is converted into a stablecoin, moved onchain, and then converted back into fiat. Stablecoin FX is broader and can also include fiat-to-stablecoin, stablecoin-to-fiat, and stablecoin-to-stablecoin conversions.

Can stablecoin FX replace traditional FX?

Stablecoin FX is unlikely to replace traditional FX. Traditional FX remains much larger, deeper, and more liquid. Stablecoin FX is more likely to develop as a parallel layer for specific use cases, such as cross-border payments, OTC settlement, treasury rebalancing, and stablecoin liquidity management.

Who uses stablecoin FX?

Stablecoin FX can be used by payment providers, OTC desks, brokers, fintech platforms, stablecoin issuers, liquidity providers, banks, and treasury teams. It is most relevant for businesses that need to move value across currencies, regions, or digital asset markets.

What infrastructure is needed for stablecoin FX?

Institutional stablecoin FX requires liquidity providers, execution venues, on- and off-ramp partners, custody or wallet infrastructure, compliance tools, settlement controls, reporting systems, and reconciliation workflows.

What are the main risks of stablecoin FX?

The main risks include liquidity risk, issuer and redemption risk, peg risk, counterparty risk, custody risk, regulatory uncertainty, blockchain network risk, and accounting or reconciliation challenges.

Is stablecoin FX regulated?

Regulation depends on the jurisdiction and the specific activity involved. A stablecoin FX flow may touch digital assets, payment services, money transmission, custody, FX, sanctions screening, and cross-border transfer rules. Institutions need to assess each corridor and workflow separately.

Why does stablecoin FX matter for institutions?

Stablecoin FX matters because it gives institutions a new way to move currency-linked value across markets. For payment providers, brokers, OTC desks, and treasury teams, it can improve settlement speed, liquidity mobility, and operational control when supported by the right infrastructure.